In 2016, the Greek debt crisis was largely overshadowed in the media by other international dramas, including the U.K. Brexit vote and the U.S. election. Nevertheless, during this period banks were increasingly optimistic regarding the country’s credit progress – following the release of EU funds in December 2015, the banks upgraded their views of Greek’s credit riskiness and the CBC* for Greece improved by a notch in March 2016. The announcement of potential IMF assistance led to a further sharp improvement and in July they moved up an additional notch. Further improvements followed in October, with good progress on the 15 structural milestones set by the EU. The rating agencies have generally maintained stable but divergent views on Greece: Moody’s has a pessimistic Caa3 rating, Fitch is at CCC and S&P moved from CCC+ to B- in January 2016.

However, at the end of 2016, the agreement for further financial assistance stalled. While the EU has plans to unlock short-term debt relief measures this month, and is still in talks with a wavering IMF over its participation, Donald Trump has brought fresh uncertainty. He is expected to push for limitations on IMF lending practices in Europe and Greece could be the first casualty. Some commentators may argue that Greece was admitted to the EU under false pretences; but a setback at this stage comes at a politically difficult moment for the EU. The monthly Credit Benchmark data will pick up any reversal in the recent positive trend for Greece; and we will shortly be reporting on Sovereign trends across the EU in the post-Brexit and post-Trump environment.

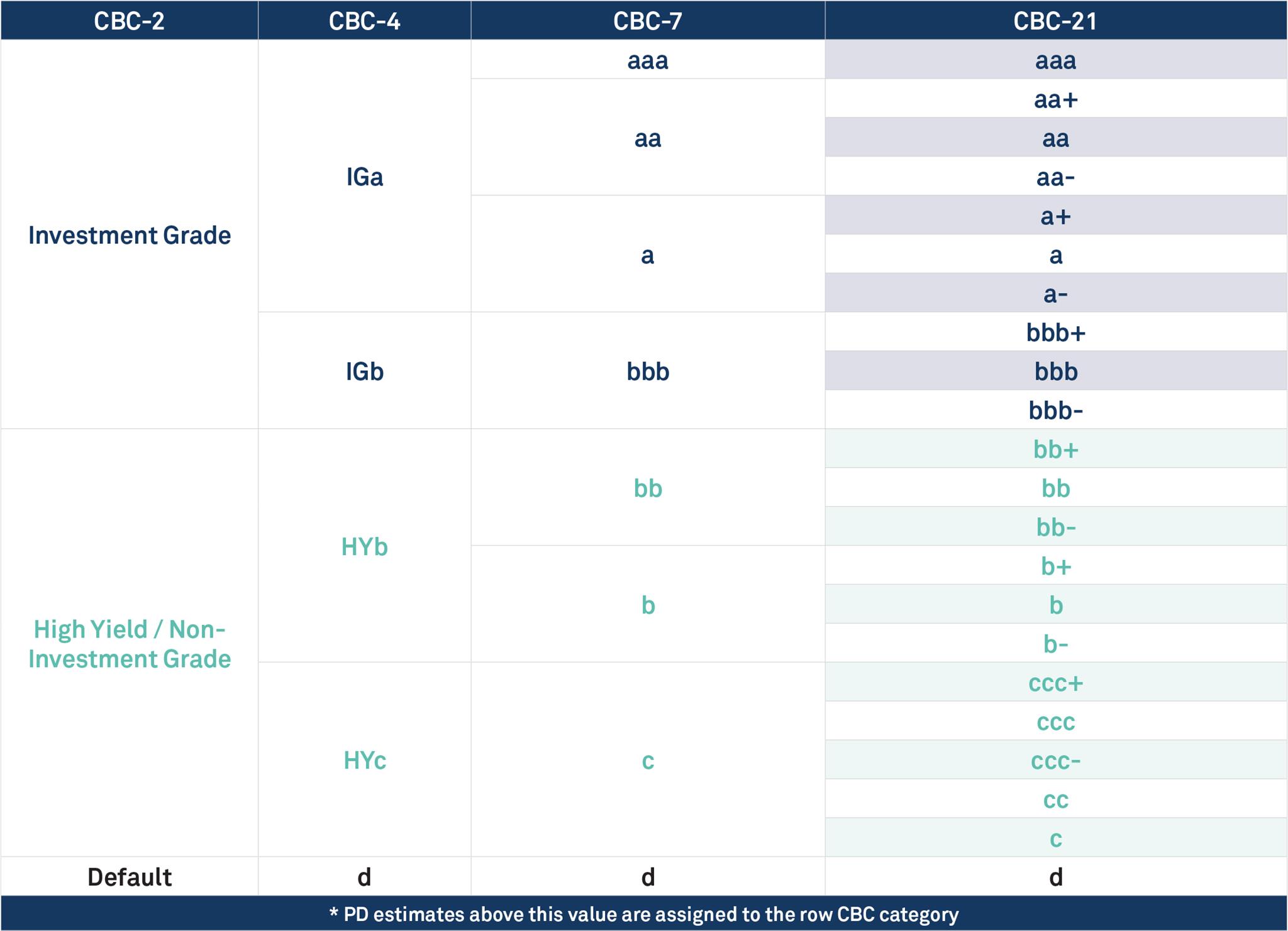

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}