The UK’s currency remains very volatile post-Brexit, but may be recovering. The country’s credit rating may suffer more permanent damage.

As yet, the credit world has been cautiously negative about the June 23 referendum on quitting the European Union. Both S&P and Fitch downgraded the UK’s sovereign rating to AA (a notch below Moody’s) just after the Leave camp’s unexpected win. The CBC* had already slipped down in March. The full impact is yet to be reflected in economic data, but the next Credit Benchmark data will be published before the end of this month and that should provide some interesting pointers.

Currency traders did not take long to make up their minds. At $1.30, the pound has fallen 13 percent against the dollar since just before the referendum. Sterling is also down 12 percent versus the euro. Most of the drop came right after the vote, but there has been another smaller drop in August before the bounce this week.

FX traders can make a good case for pound pessimism. To start, the Bank of England’s aggressive monetary policy is clearly unfriendly to Sterling. With both more monetary stimulus and a higher inflation rate on the way, UK probably offers the worst potential real return on short term government debt of any major economy.

Then there is the probability that the country’s growth prospects have deteriorated – generally bad for a currency. Finally, the UK’s large current account deficit – about 5 percent of GDP for each of the last three years – has become riskier. Foreigners may hesitate to invest or buy property, and there is the outside chance that a poor settlement for London’s financial trade might create an outward migration of capital – disastrous for the pound.

Still, the FX markets, which have a strong tendency to overshoot and reverse, may have already adjusted fully to the referendum vote. It may even have gone too far. Expectations for the UK economic are now low, so even modestly good news would support sterling. If Brexit turns out to be a very slow and very partial decoupling, the pound could rise substantially.

The damage to the sovereign risk will not be so easily repaired. The decision to call the referendum, the government’s inability to prevail in the vote and the feeble and incoherent response to the ‘leave’ victory have durably damaged the reputation of Britain’s political institutions. Also, Brexit uncertainty is likely to lead to at least a few years of slower GDP growth than previously expected. That will add to the burden on the state pension system and to the risk of populist measures which reduce fiscal strength.

The risk of a British sovereign default will remain minimal, even if the rating slips down a few more notches. Unlike companies, governments can usually use higher than expected inflation to increase revenues and keep up interest payments, and the authorities can usually cajole banks to roll over debts. Still, the decline in ratings reflects something real and economically damaging. The British government has become less reliable. That won’t change soon, whatever happens to the pound.

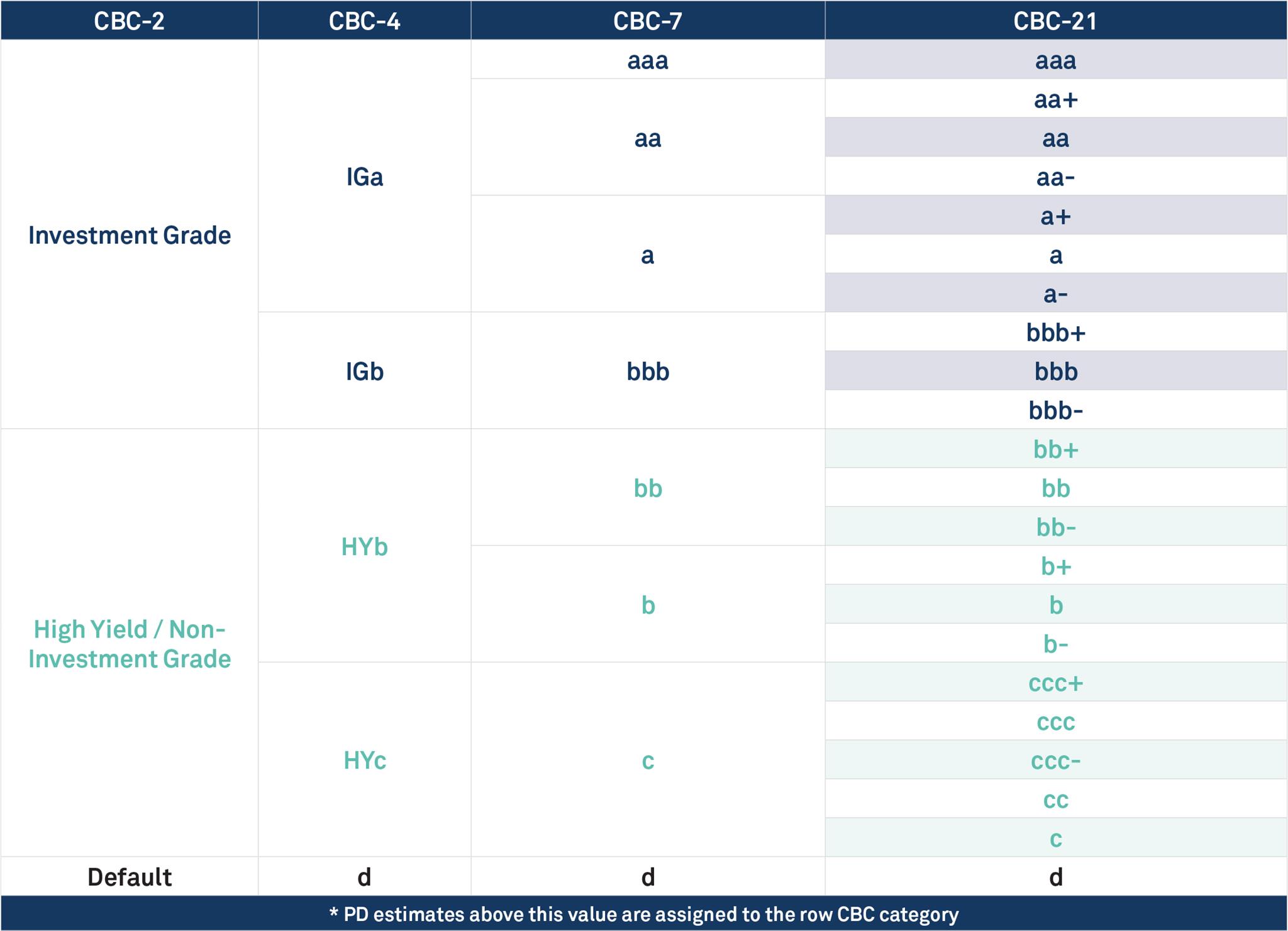

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of [bbb+] is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}