Big Tech is having a rough time in 2018. After providing about a quarter of the 2017 stock market gains, the recent #techlash against Silicon Valley has seen Senators grilling Facebook CEO Zuckerberg, and President Trump calling out Amazon for alleged abuse of the US Postal Service. The privacy and anti-trust issues raised have also focused public concerns on Google (Alphabet), Apple and New Tech in general; tougher regulation may be on the horizon. In this environment, some investors have turned to “Old Tech” (Intel, IBM, Microsoft etc) and even traditional, non-Tech companies as safe havens. Although – ironically – Zuckerberg’s handling of the first day of Senate Committee questions actually increased his personal wealth by about $2bn thanks to a Facebook price rally.

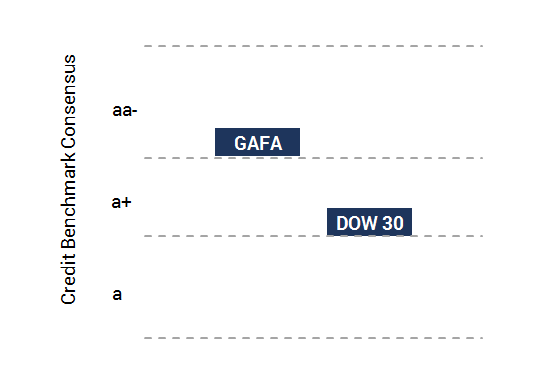

The chart below is based on bank-sourced data.

The four GAFA giants (Google, Apple, Facebook and Amazon) currently have a healthy average CBC* of aa-, whereas the Dow 30 has an average of a+. The CBC for the Dow is very close to a if Apple is excluded. But current administration rhetoric favours traditional American businesses, like Coal and Steel; and this has already had a positive effect on credit (see The Trump Effect). Big Tech has seen off the threat of increased regulation before now, but there is scope for the credit gap between Old and New Economies to narrow.

*Credit Benchmark Consensus (“CBC”): this is a 21-category alphanumeric scale based on bank-sourced one-year probability of default estimates. It is similar to the scale used by the main credit rating agencies, so that a CBC of bbb is approximately equivalent to BBB reported by S&P and Fitch, and Baa2 reported by Moody’s.