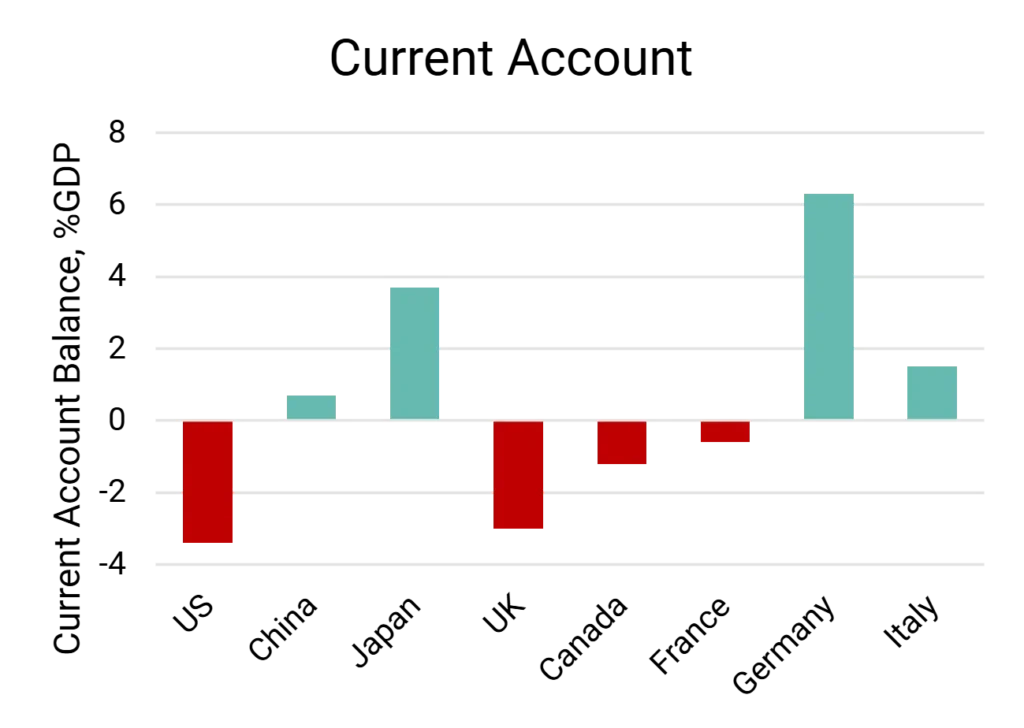

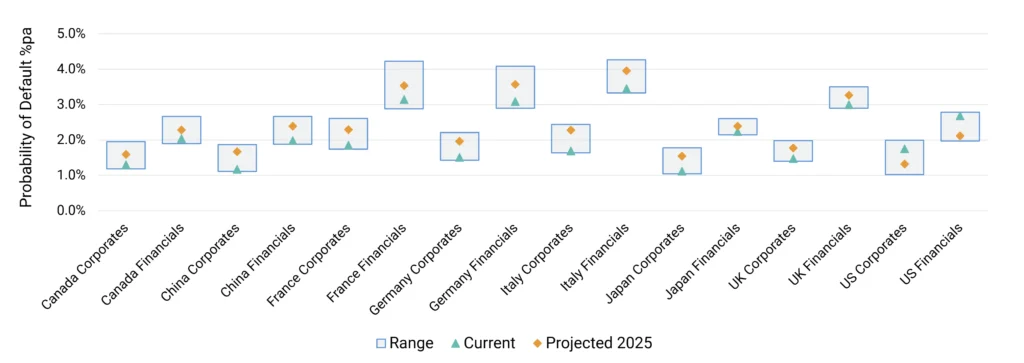

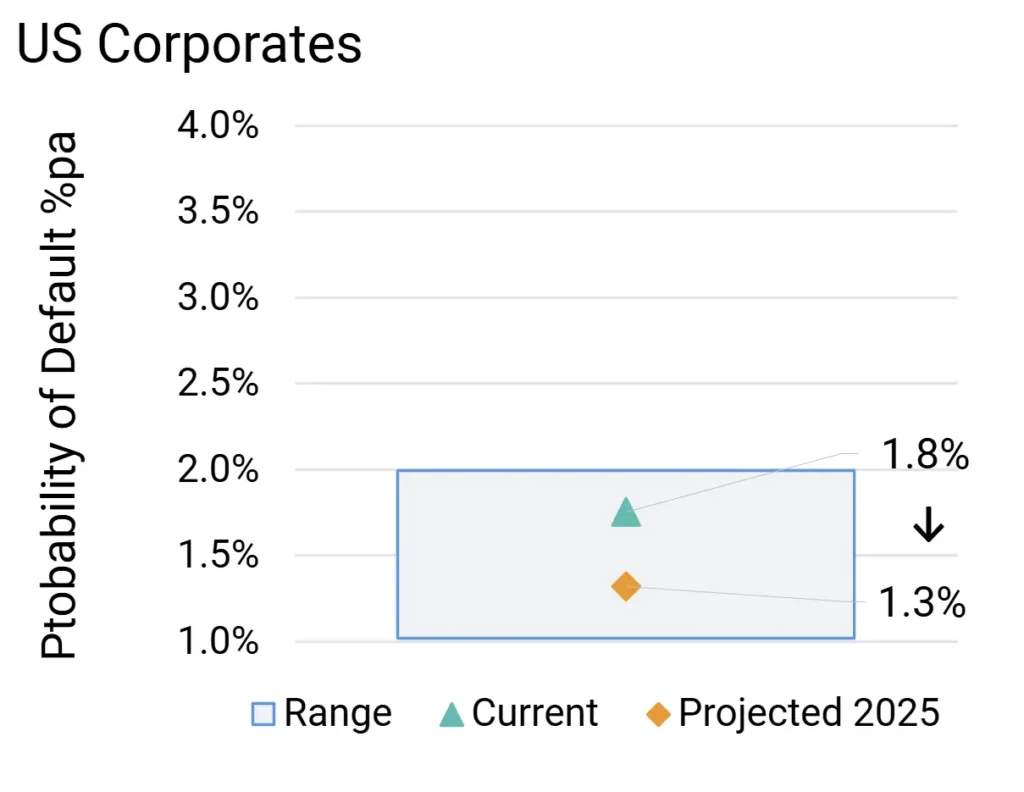

The US economy remains strong and long-term real rates are moderate, but a growing current account deficit strengthens the case for protectionism. Tax cuts will boost growth, but lower US short rates and higher import tariffs are inflationary despite lower oil prices. Tariffs will hit all major US trading partners, but UK and Japan are more vulnerable than EU economies.

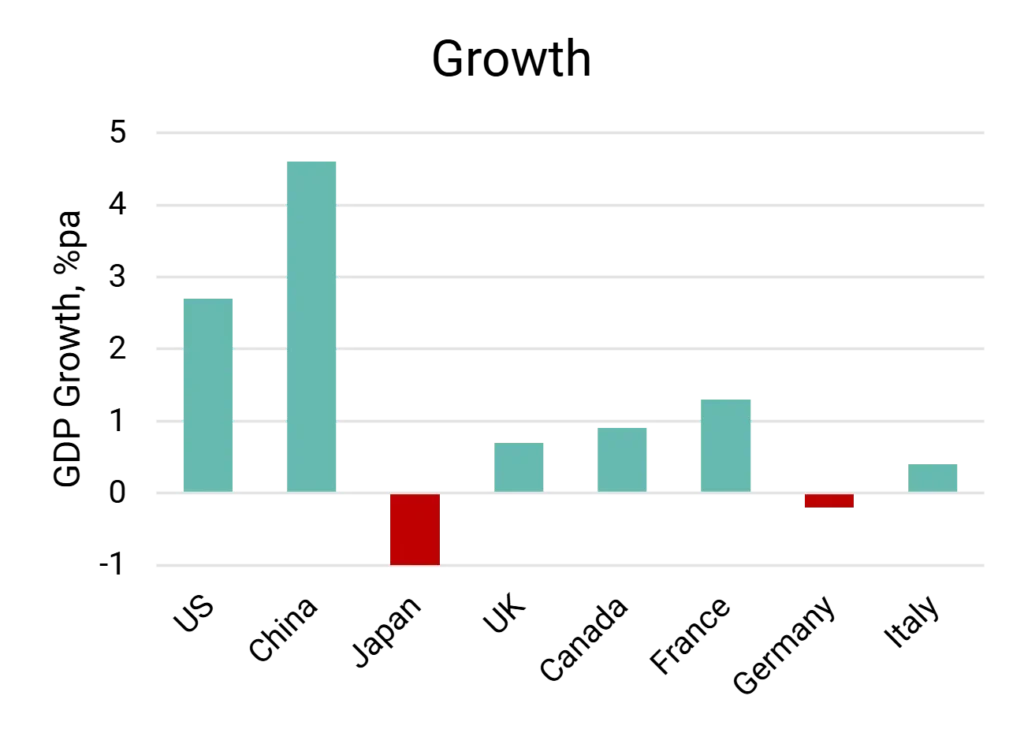

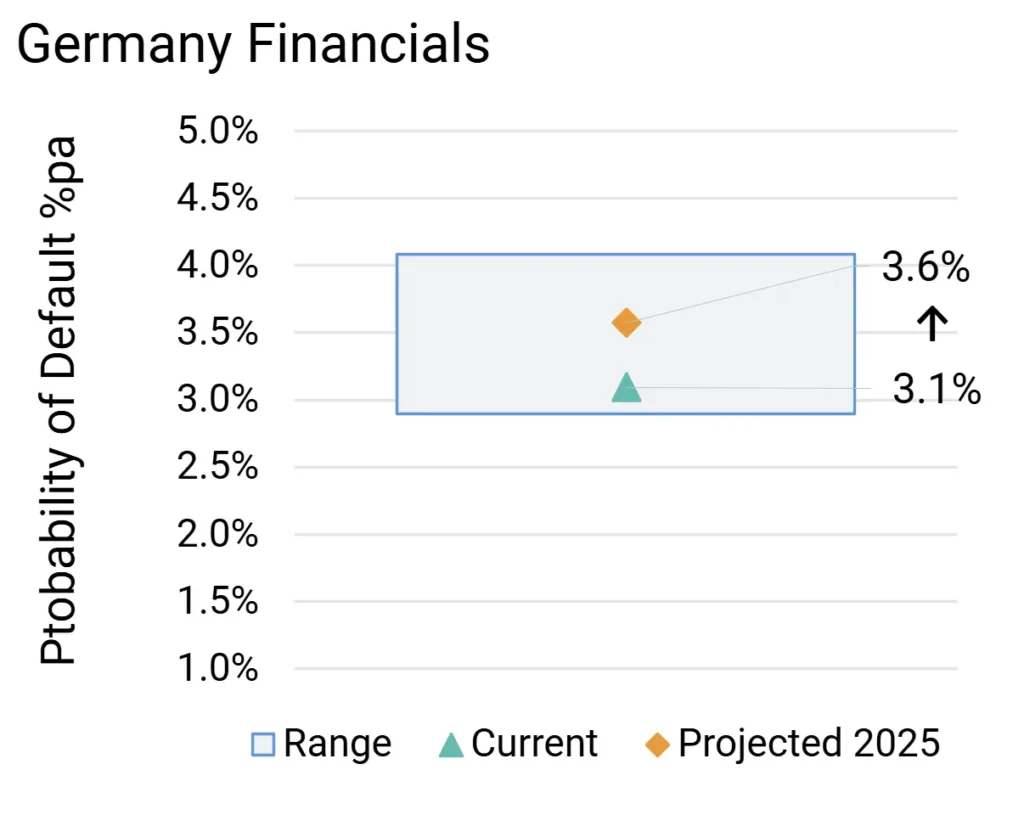

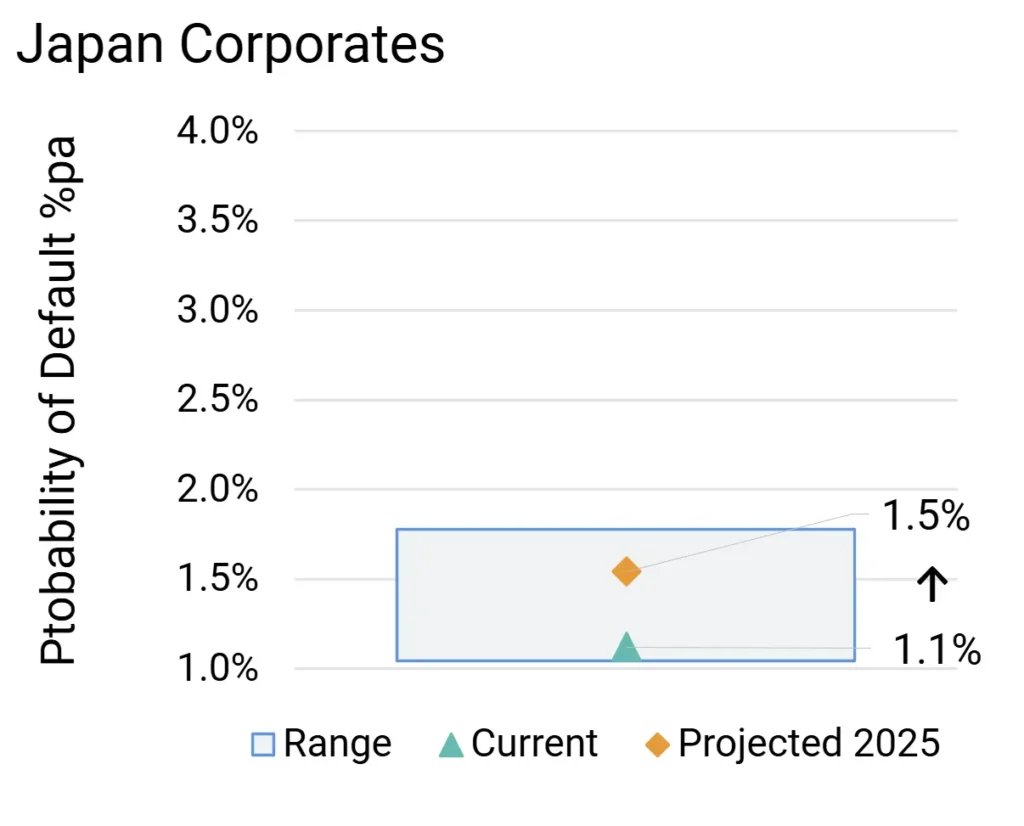

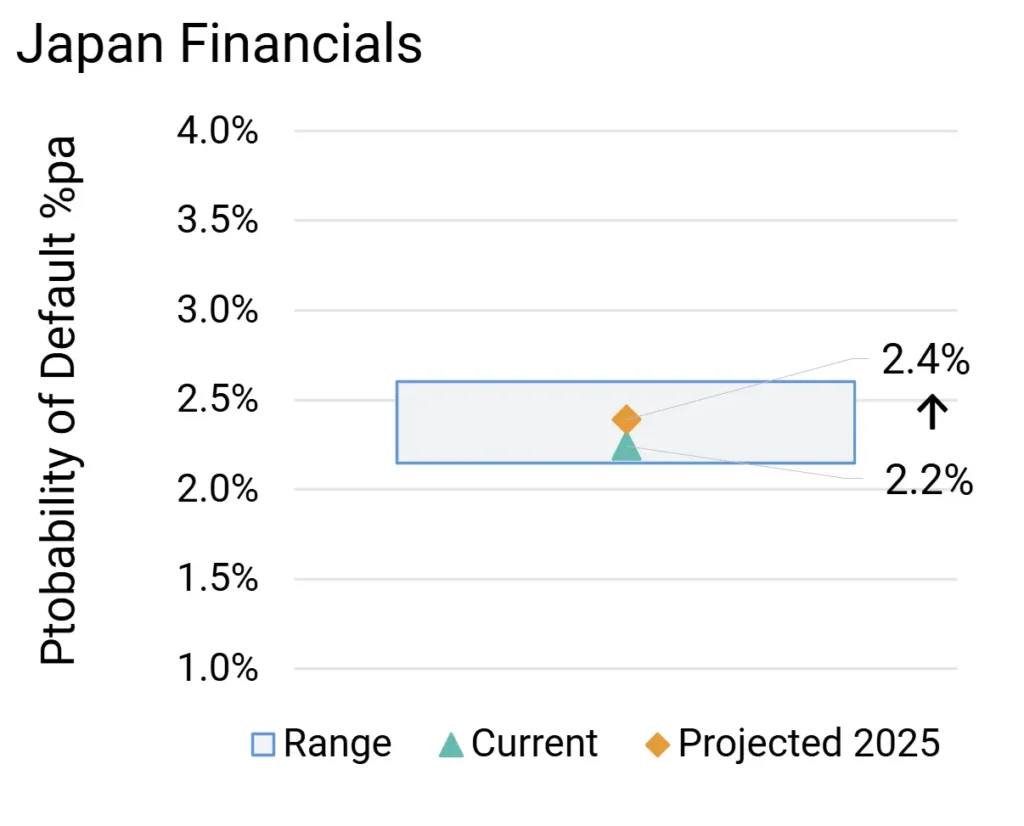

Japan and Germany face high inflation, shrinking Current Account surpluses if tariffs hit exports and growth rates, and both have a growing defence burden.

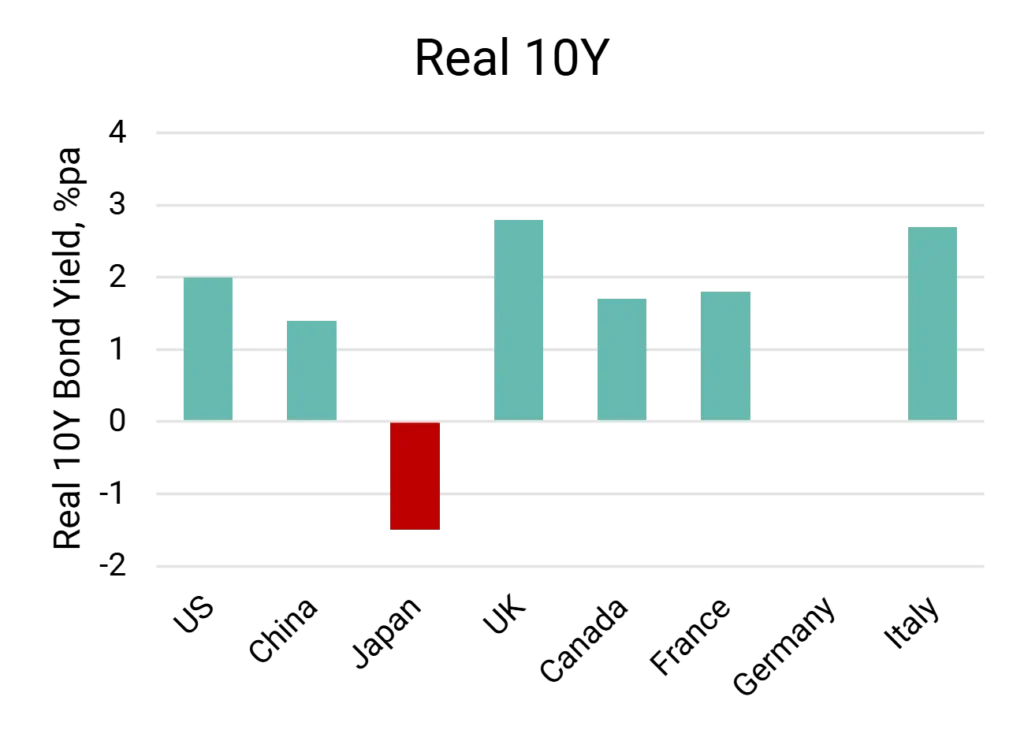

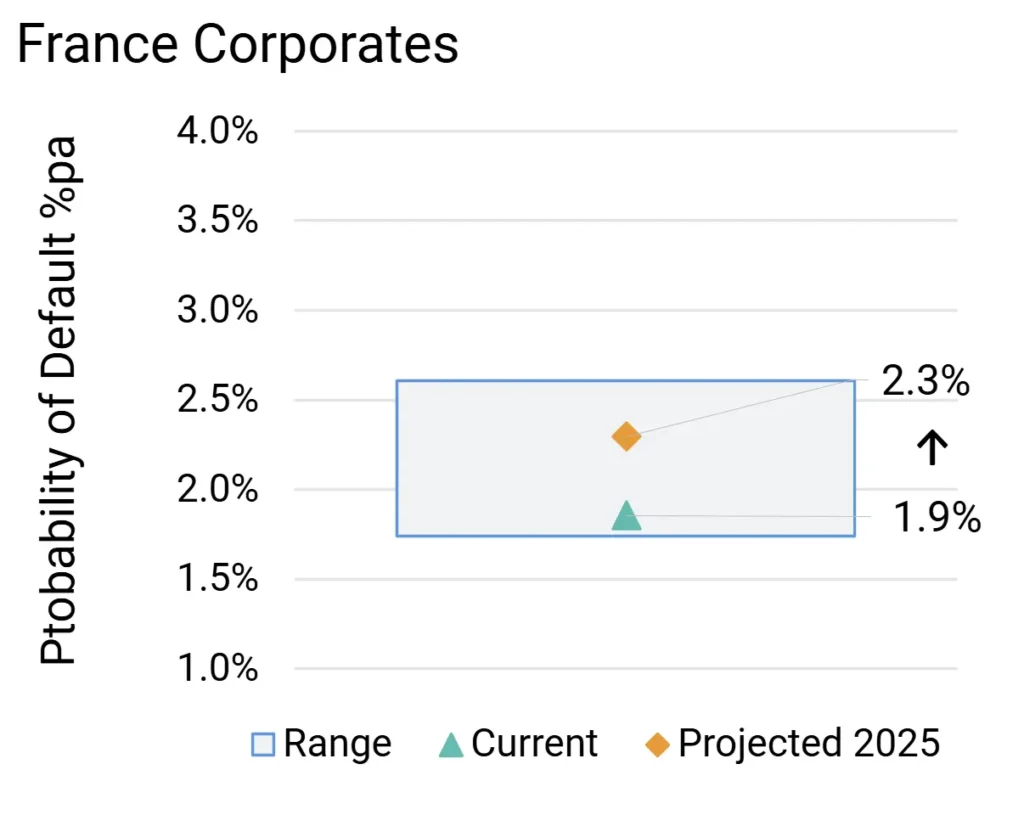

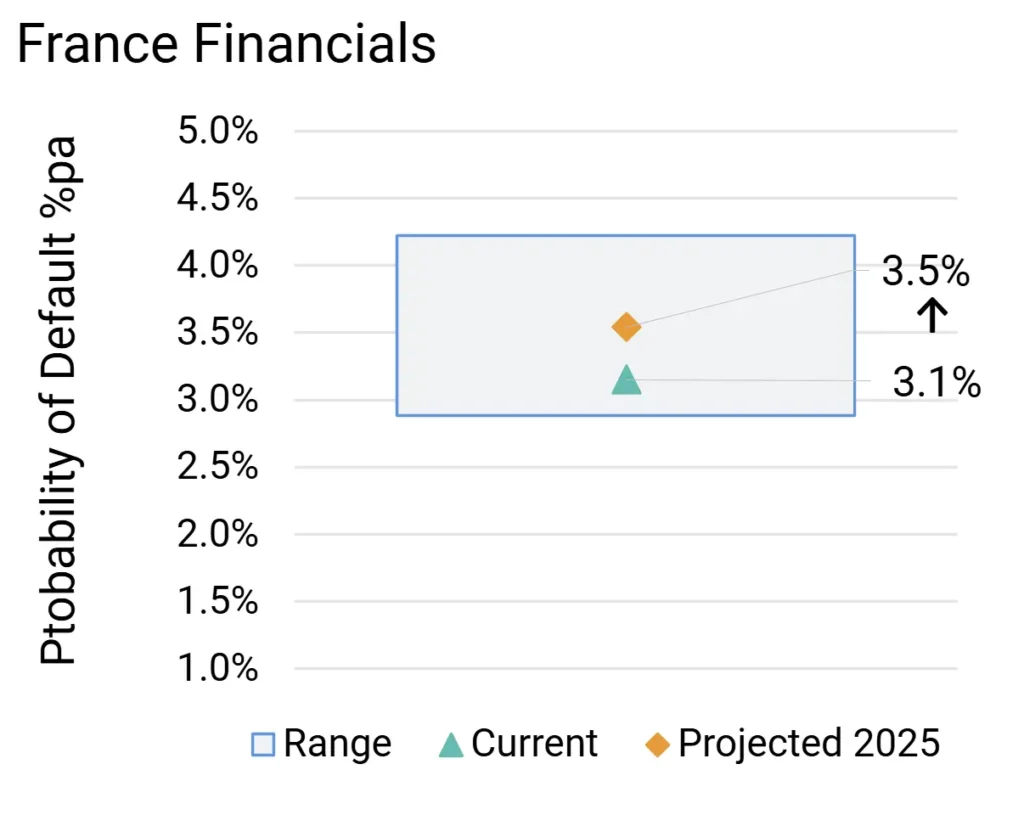

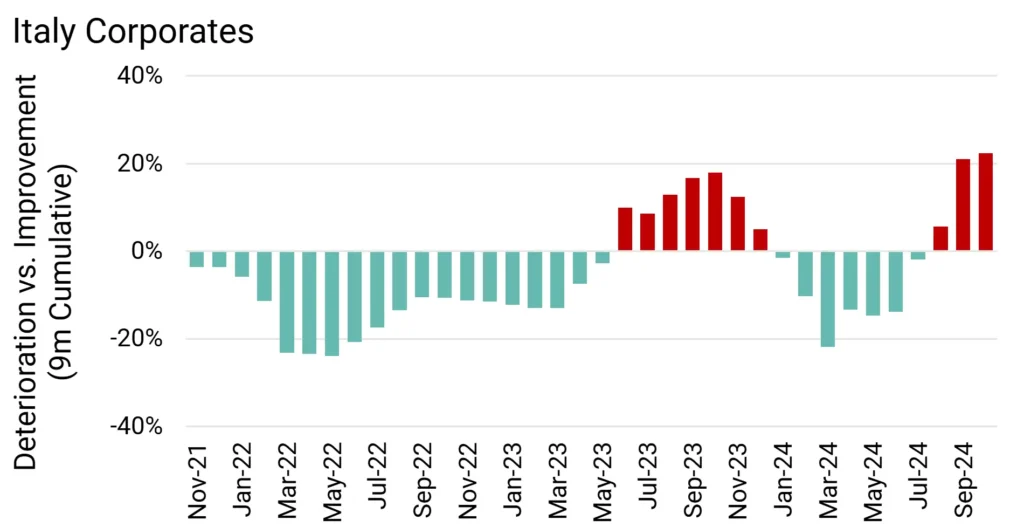

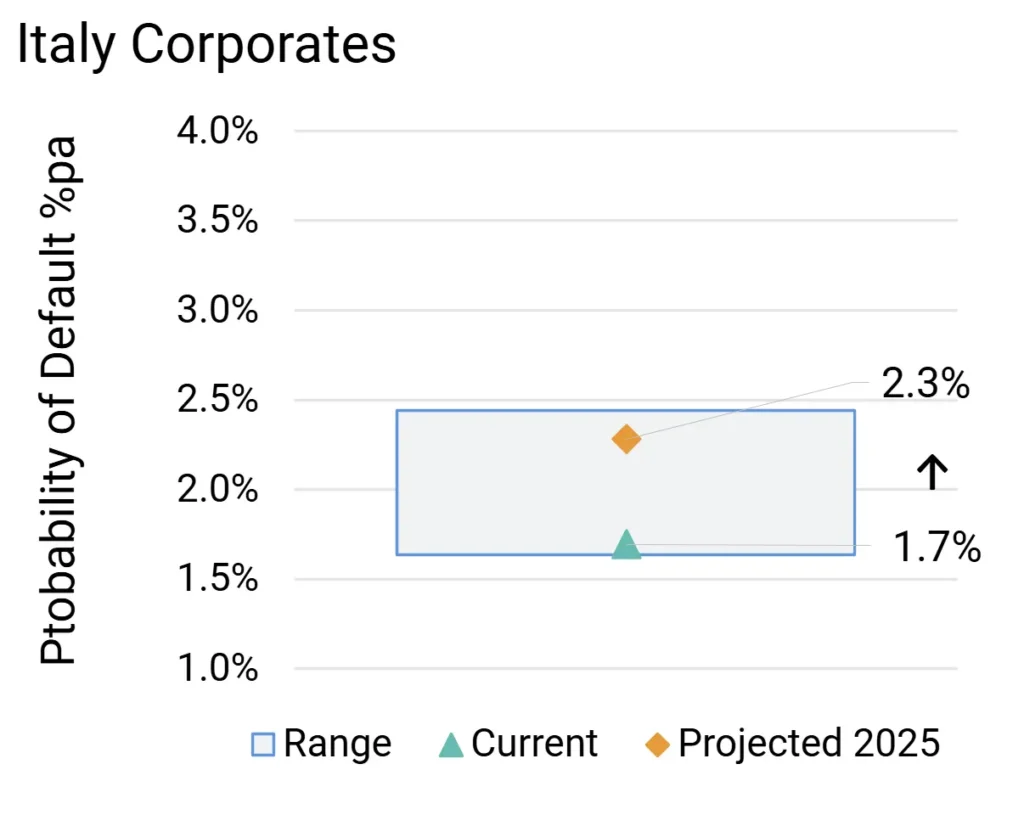

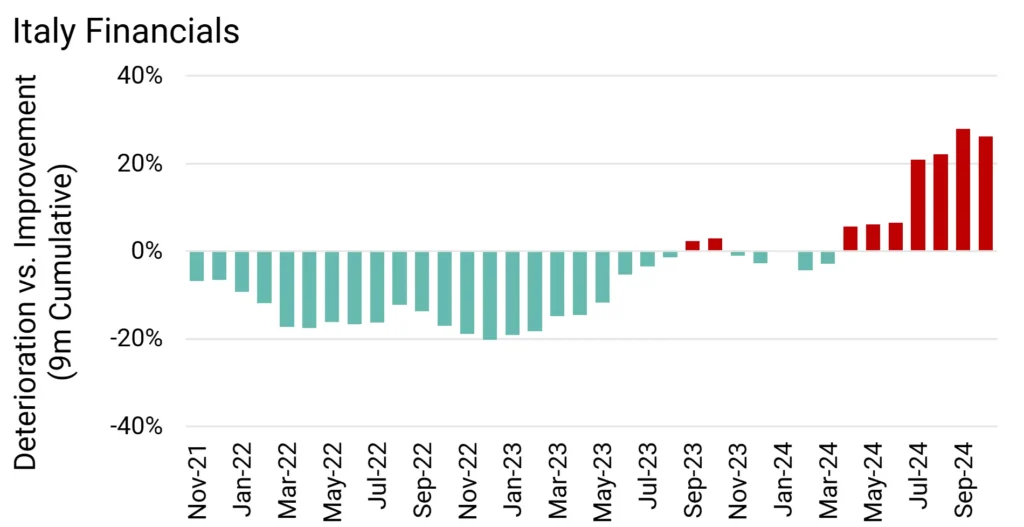

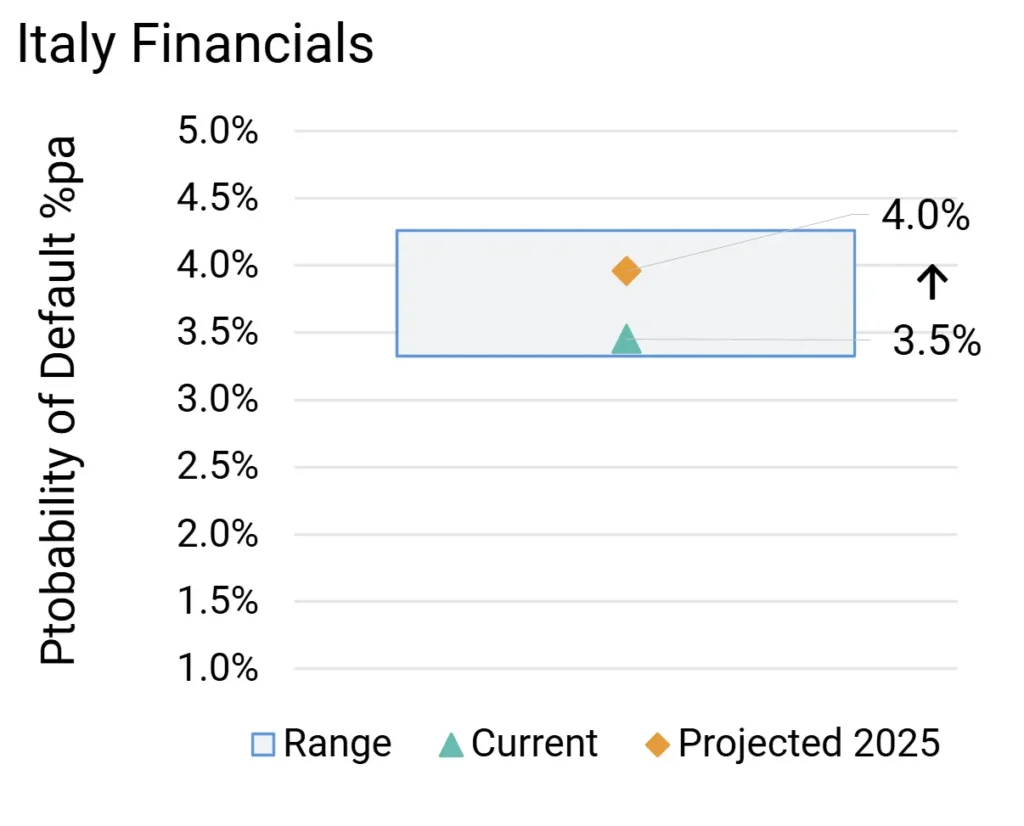

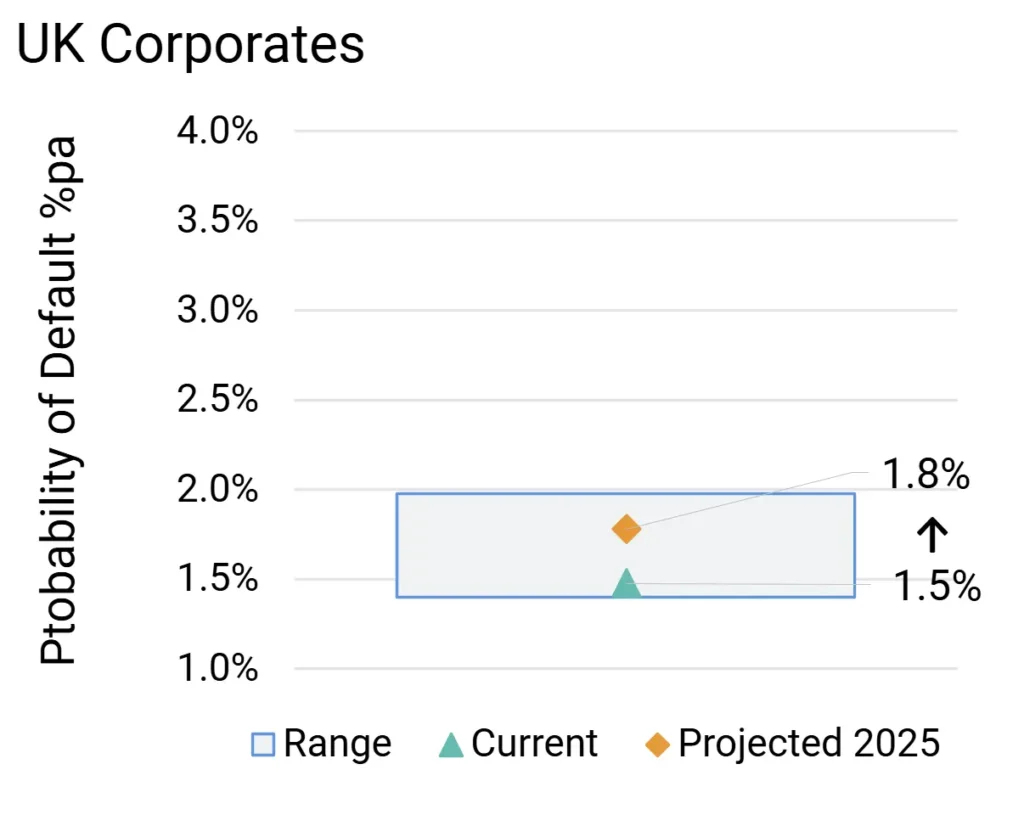

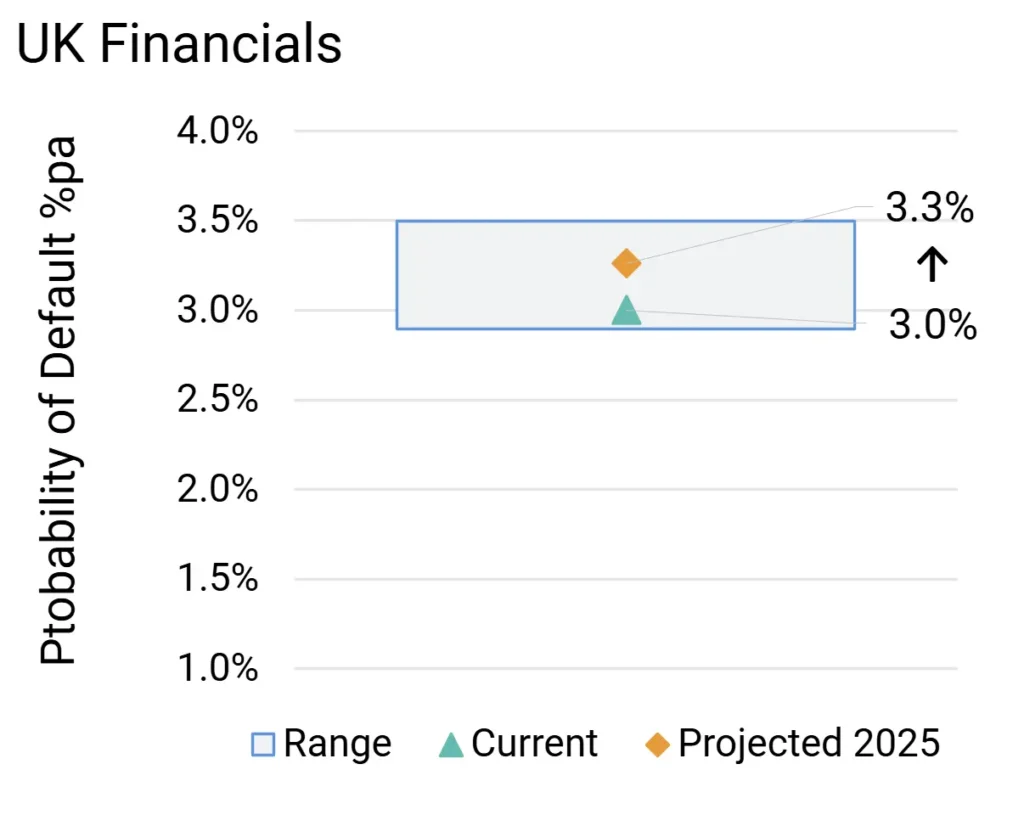

Italy has a current account surplus, thanks to strong Asian demand for luxury goods plus low dependence on Russian gas. It also runs a primary fiscal surplus, although its historic Sovereign debt load keeps real borrowing rates high. France has similar long term real rates as the US and a mid-range current account deficit, but sluggish growth and political paralysis. The UK’s weak current account and LDI crisis hangover have left it with high real rates but some scope for monetary easing; partly offsetting its vulnerability to trade shocks.

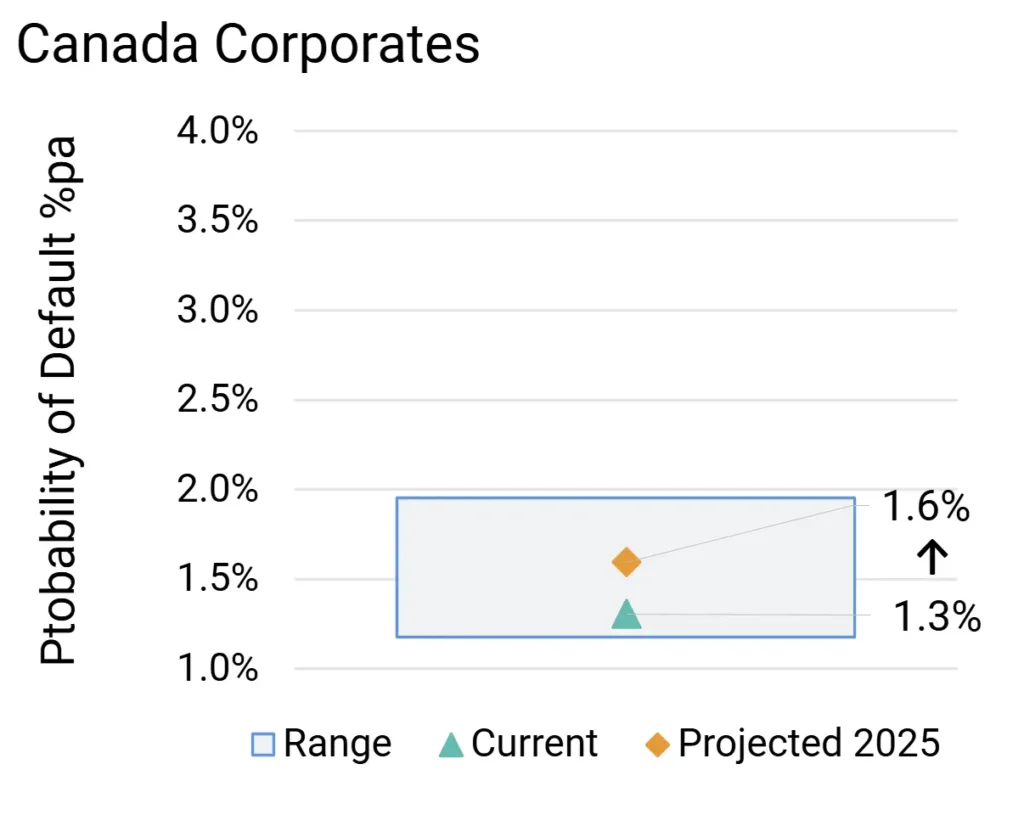

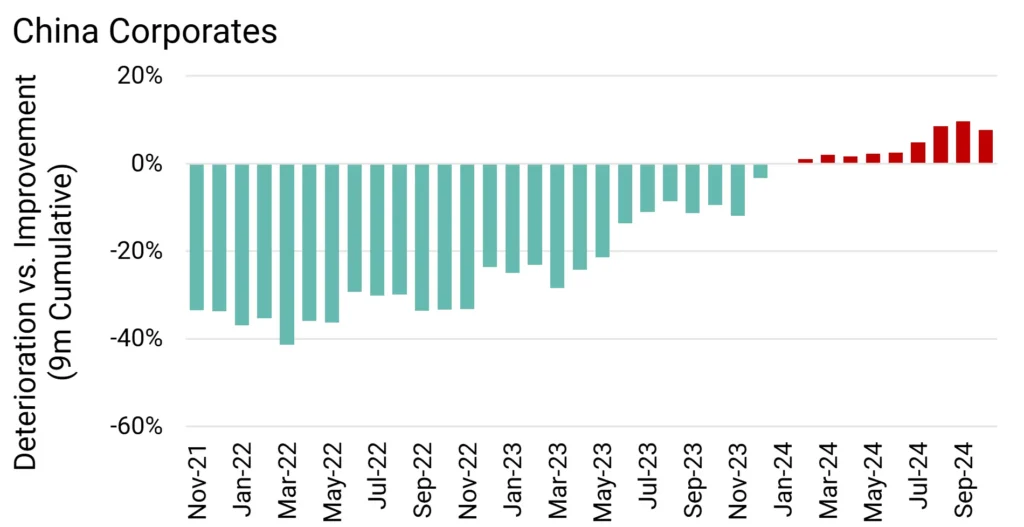

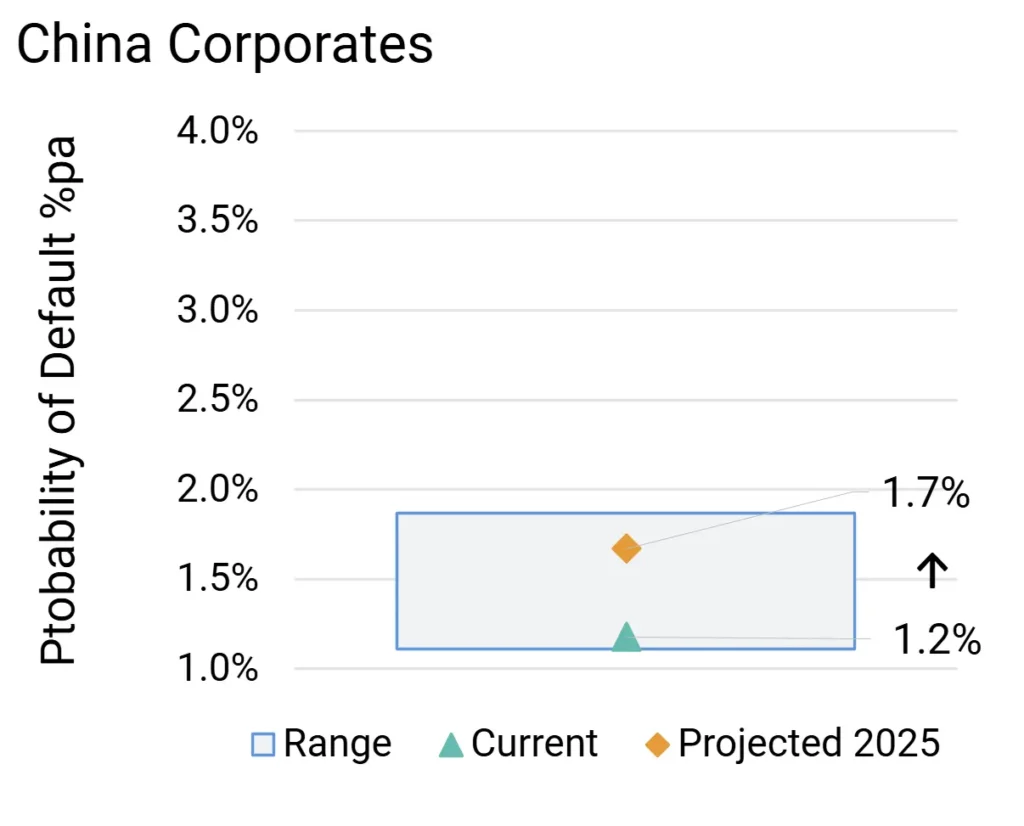

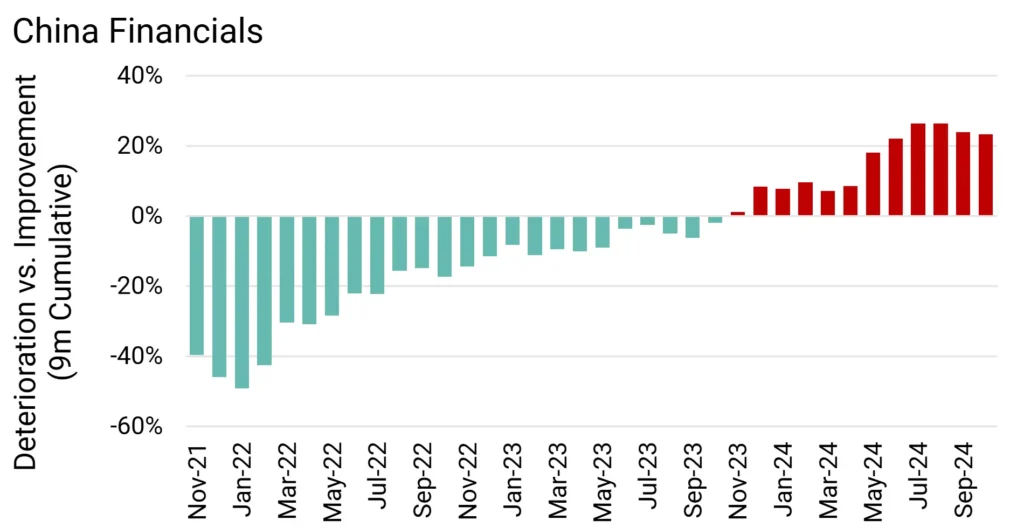

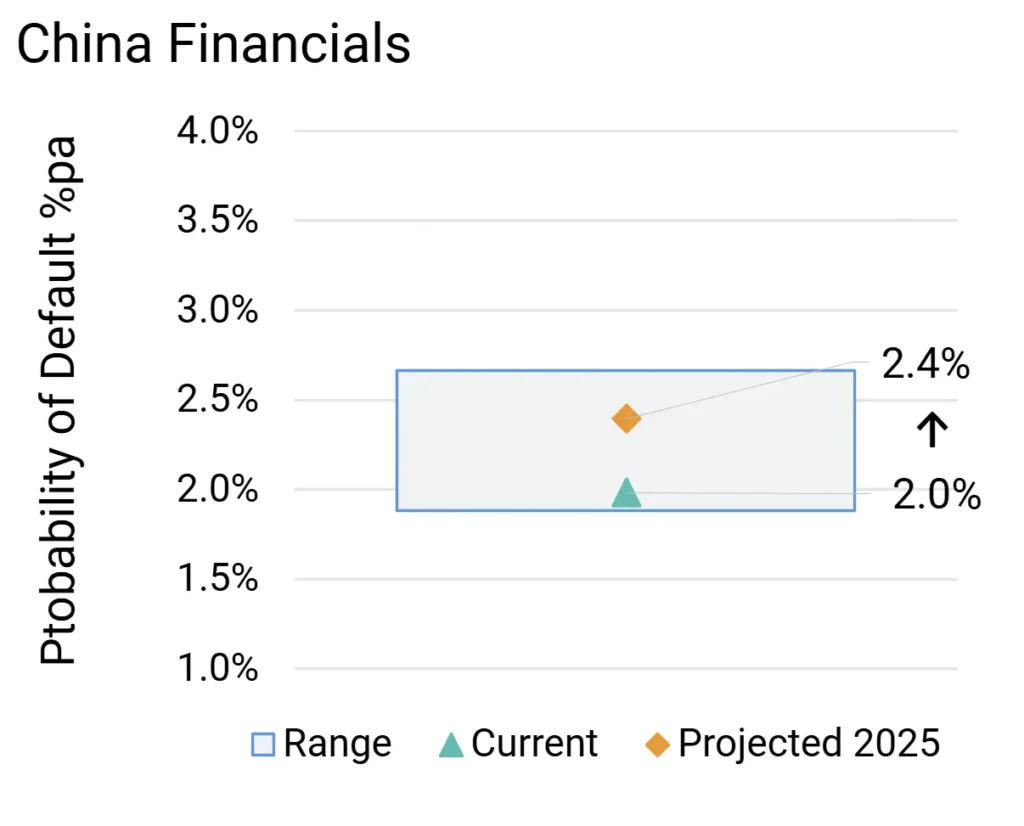

China’s strong but below-trend growth rate follows the domestic real estate bust, despite various fiscal stimulus packages. As the world’s largest oil importer, it will benefit from lower oil prices but faces exceptionally high US tariffs in 2025 – negative for China’s traditional role as global credit supplier, positive for various other countries. Nomura lists the main winners from Chinese trade diversion as Vietnam, Chile, Malaysia, Argentina, Hong Kong, Mexico, Korea, Singapore, Brazil and Canada – so Canada may gain here as well as lose from tariffs.

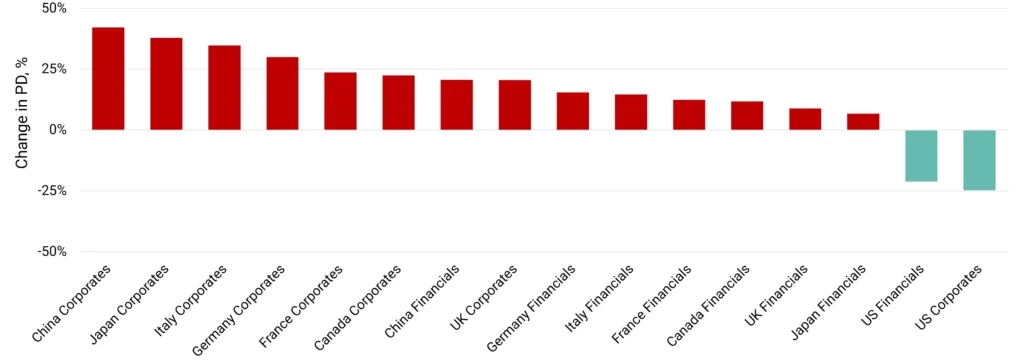

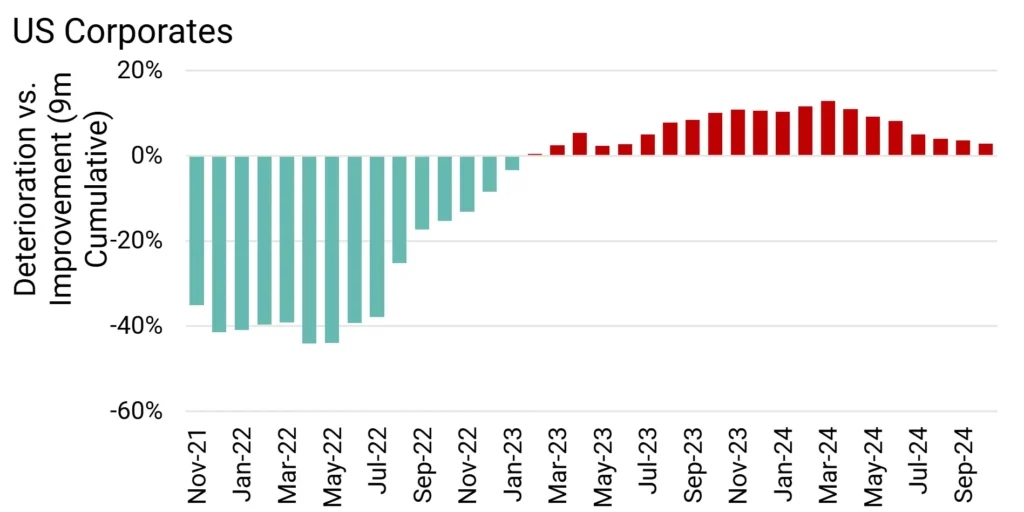

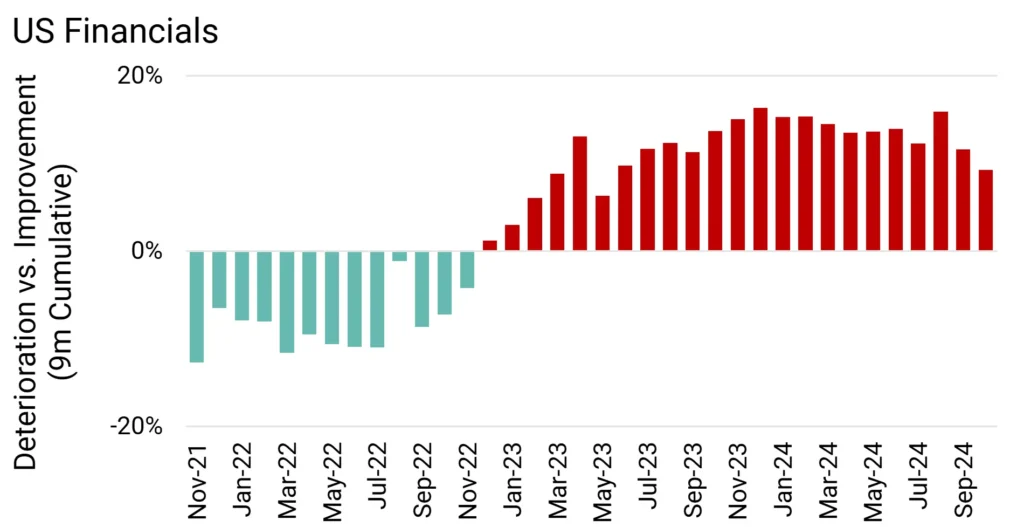

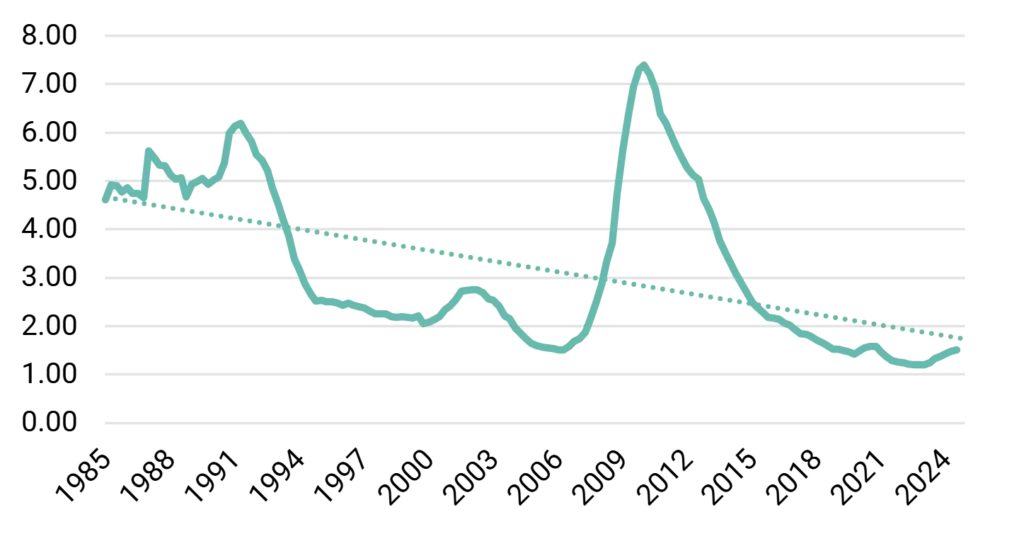

Major shifts in trade and regulation and shifts in the technological and corporate landscape will have some impact on default rates. But even extreme events can have a surprisingly mixed effect on overall default rates. See appendix for chart showing the 40-year track record for loan delinquency rates across US Commercial Banks.

Scott Bessent as Treasury Secretary may shift policy emphasis to tax cuts and financial de-regulation. During Trump’s last term in office the US economy grew by 2.7%; tax cuts helped, although they also boosted the deficit – and Citadel economists expect another round of tax cuts to increase the deficit back to Covid levels. The IMF expect global growth to dip by 0.8%. The CEBR expect the UK to lose about 0.2% pa due to US trade policy, and UBS predict 0.5% off growth in China.