2020 was the year of the homebody. While those preferring the great indoors may have relished a government-mandated excuse to stay at home over the weekends, social butterflies and live entertainment enthusiasts struggled during months of enforced lockdowns. But how did the longer-term credit fortunes of jigsaw makers and theatre producers compare before COVID – and is a shift in leisure habits likely to persist?

With live music, mass sporting events and other leisure services curtailed for many months, consumers were forced to pursue new forms of personal entertainment and recreation. Sales of home gym equipment skyrocketed in 2020, with exercise bikes increasing in popularity by 2000% in the UK. Spending on video games grew to $56.9bn in 2020 in the US, a 27% increase from 2019.

This COVID-prompted shift towards personal leisure and recreation activities bucks a longer-term trend in the opposite direction. The growth of ‘experiences’ has been fuelled in part by the rise of social media, and from the status afforded to those boasting a life well lived – in preference to the accumulation of things. As noted in a Deloitte study on UK leisure consumers in 2019, ‘…spending on things to do has grown so much faster than spending on things to own.’

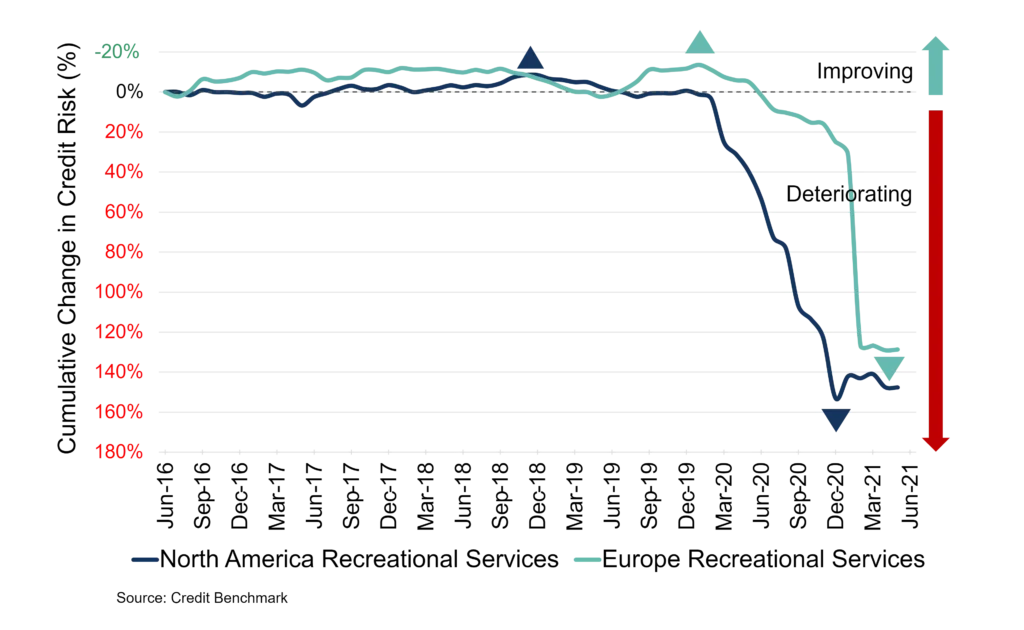

This preference for experiences and live entertainment is reflected in the consensus credit trend of North American and European Recreational Services companies over the past 5 years.

Figure 1: Credit Trend – Recreational Services

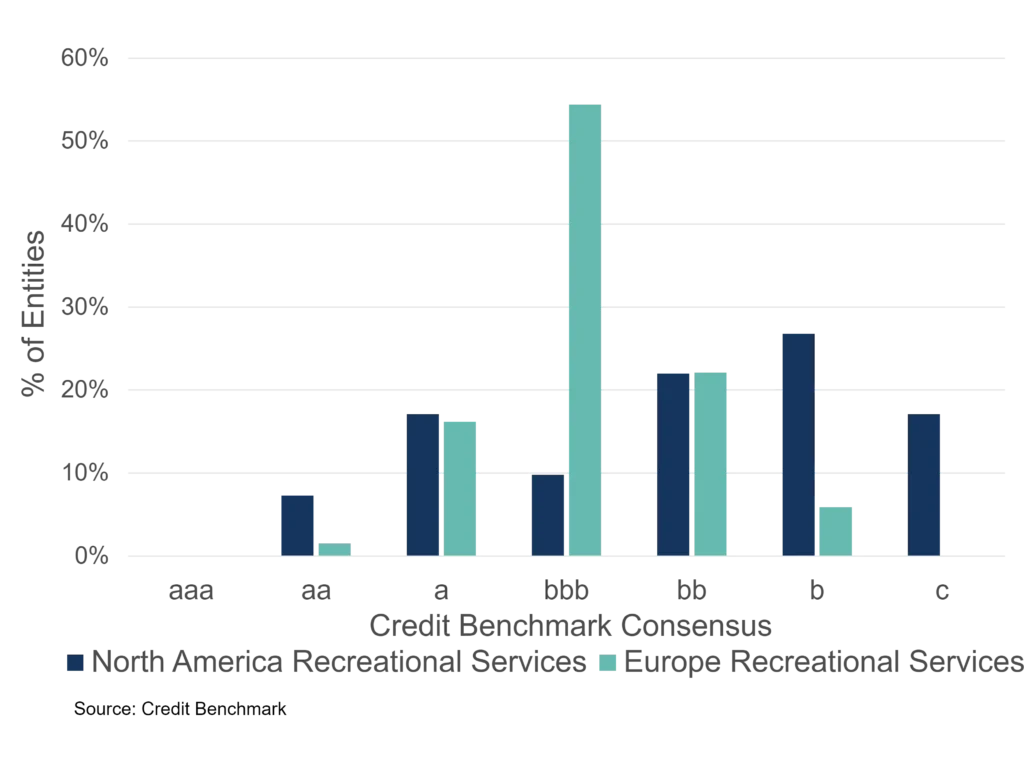

Figure 2: Credit Level – Recreational Services

Some examples of recreational services companies listed in this analysis include gyms (Gym Group PLC, Fitness First, Virgin, Goodlife), sporting clubs and leagues (Liverpool Football Club, PGA Tour Europe, Major League Baseball, NBA), stadiums and arenas (Wembley National Stadium, Las Vegas Arena), entertainment providers (Live Nation, Cirque de Soleil), theatres and cinemas (Everyman Media Group, Cineworld, AMC), and museums and galleries (Metropolitan Museum of Art, The Kennedy Centre).

The long-term trend for both regions shows relative stability between mid-2016 and March 2020, at which point things went rapidly downhill for obvious reasons. Though European firms at first declined at a slower pace than US firms, a severe drop in early 2021 – perhaps in response to a fresh round of Christmas lockdowns – saw them reach similar footing. Both groups plateaued from March onwards and have remained fairly stable. The credit level chart shows a somewhat even spread across the credit categories for North American companies, while European firms are vastly overrepresented in the non-investment grade category of bb, and almost none fall within the higher quality aaa to a categories.

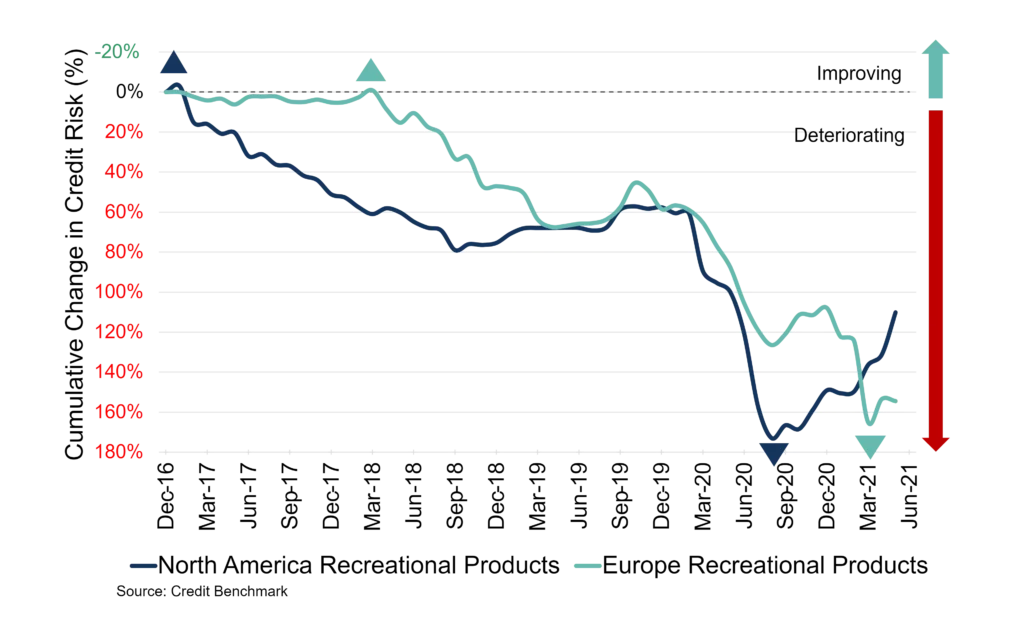

The consensus credit trend for North American and European Recreational Products tells a different story.

Figure 3: Credit Trend – Recreational Products

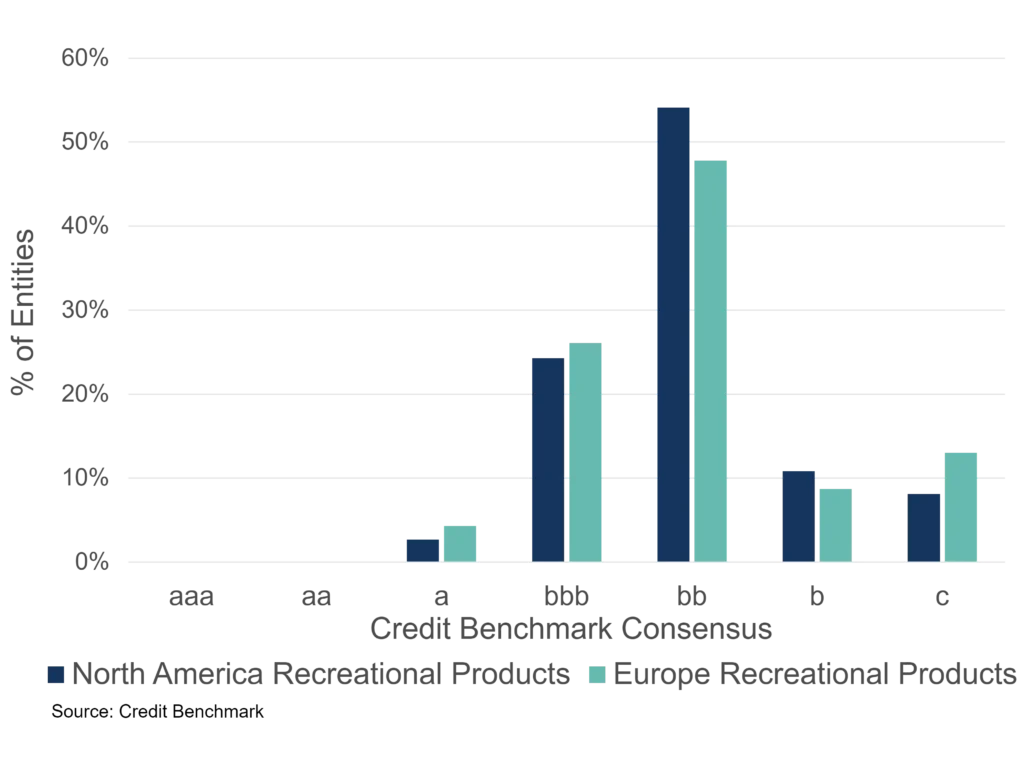

Figure 4: Credit Level – Recreational Products

Some examples of recreational product companies listed in this analysis include manufacturers of bicycles (Giant, Shimano), toys and games (Lego, Hasbro, Mattel, Wizards of the Coast), sporting gear (Nike, Dicks Sporting Goods, Wilson Sporting Goods), pool companies (Pool Corp), and boating and fishing gear (Daiwa Sports, Bass Pro).

These firms have seen a steady decline for some time, with the North American companies on a negative trajectory since tracking began in early 2017, and the European companies again trailing but ultimately following the same trend from early 2018. Some improvement in the North American companies between late 2018 and early 2020 saw the two groups converge before both were hit by the COVID effect (leisure good manufacturers are not immune from widespread supply chain disruptions). The regional divergence is apparent once more as North American companies began to improve in mid-2020 (perhaps buoyed by the renewed interest and spending on personal leisure) and have shown significantly improved fortunes since this point. The European companies lag but recent data indicate that the group may be following the same path of improvement. The credit level chart shows that Products are generally worse rated than Services, however the distribution between regions is a lot more even. The majority of companies for both groups lies within the non-investment grade bb category.

Consensus credit data, sourced from 40+ leading global financial institutions, demonstrates that companies offering leisure products are generally of lower credit quality than services companies, and were already in decline before COVID impacted both groups heavily. However, the boost in spending on leisure products over 2020 and into this year has set North American companies on the path of recovery, with European firms likely to follow suit. With live entertainment and leisure services still on hold or severely hamstrung across most of the world, this pattern may continue over the course of 2021.