Numerous studies have shown that female-led companies outperform male-led companies on metrics ranging from stock price momentum and returns, profitability increases and employee satisfaction. Venture capitalism-backed firms with female founders or predominantly female leadership groups have been found to sell or go public faster, and at higher valuations. Despite this, VC funding for female entrepreneurs fell as a percentage of overall investment during the pandemic, while total VC investment grew. New analysis from Credit Benchmark suggests that female-led companies are also a better credit risk, particularly in times of economic turmoil.

Women continue to be perceived as less suitable for leadership roles than men, with a survey showing that only 69% of US-based respondents reported feeling ‘very comfortable’ having a woman as the CEO of a major US company. This percentage fell to as low as 39% across other G7 nations, and there has been little to no growth in the positive perception of female leadership since the survey began in 2018.

Consensus credit risk data, based on the collated views of expert analysts from leading global financial institutions, supports the evidence that female-led firms perform better – and are considered less of a credit risk. Analysis on the data also shows that companies with a woman in charge weathered the storm of the pandemic with greater success and demonstrated a smaller increase in the probability of defaulting than those run by men.

6% of CEO positions at S&P500 companies are currently held by women. Credit Benchmark provides a Credit Consensus Rating (CCR) for 87% of these female-led companies.

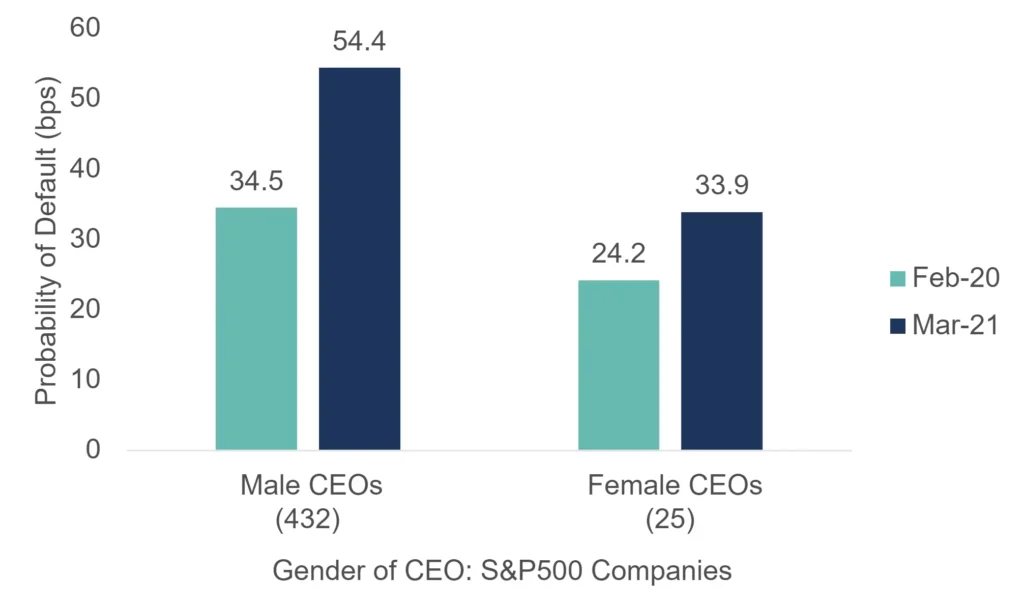

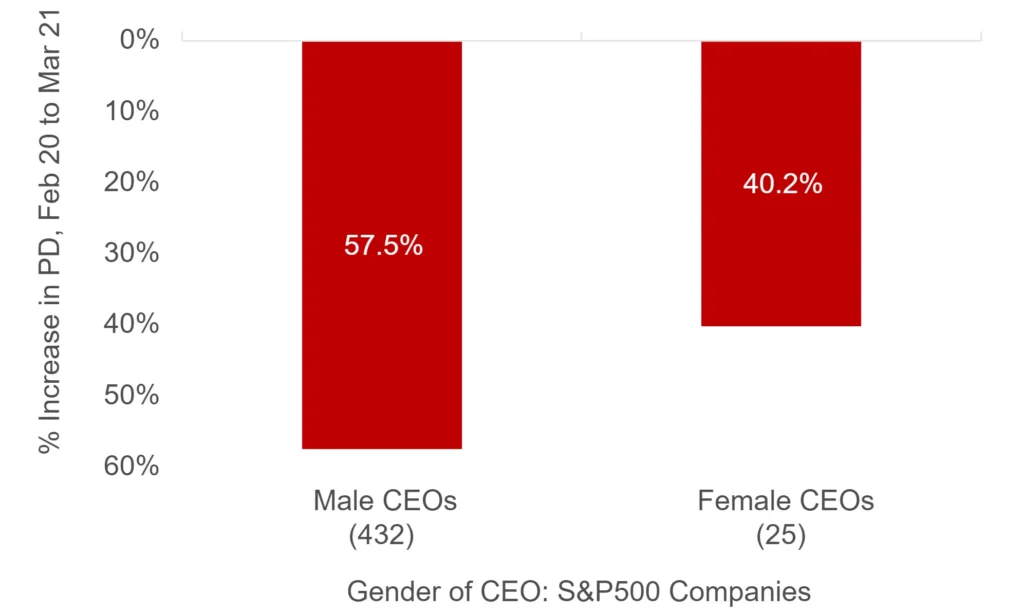

Figure 1: COVID-19 impact on Female / Male CEO S&P500 companies

The left chart in Figure 1 shows that the female-led S&P500 companies entered the pandemic in February 2020 with a lower probability of default (24 bps vs 35 bps for the male-led companies), and though both cohorts were negatively impacted by COVID-19, the male-led companies also increased in risk by a larger margin. The right chart shows that the probability of default for the male-led companies increased by 17% more between February 2020 and March 2021.

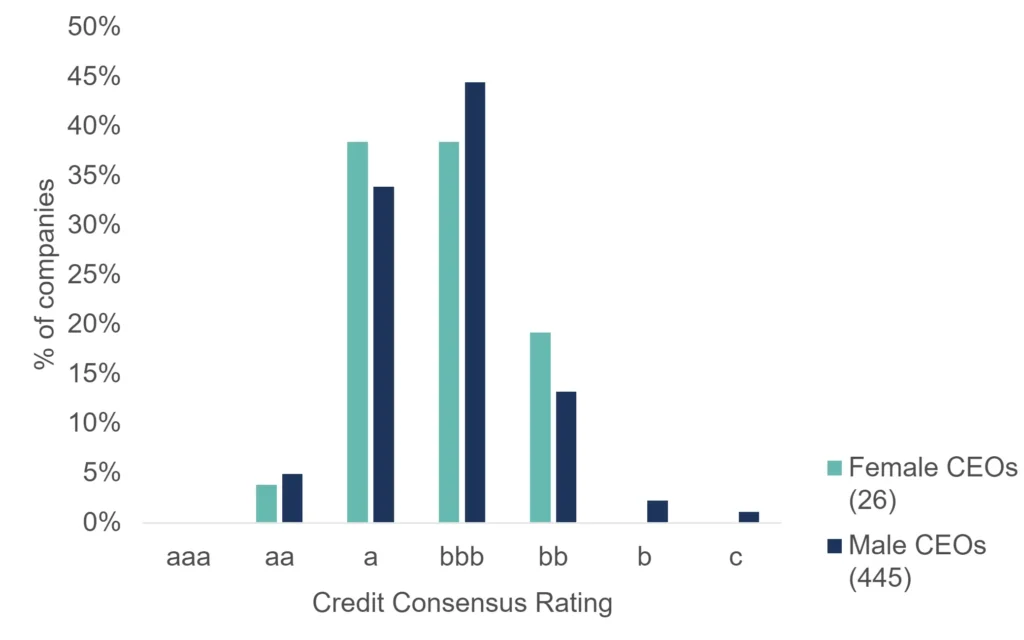

When comparing the credit risk distribution for female-led and male-led S&P500 firms (as seen in Figure 2), the data also shows that the female group have on average better credit quality, dominating in the higher a category. The male group skew more towards the lower credit categories, with the largest number of entities in the bbb category, trailing off into the lowest rated b and c categories, which contain no instances of the female CEO firms.

Figure 2: Credit Risk Distribution for Female / Male CEO S&P500 companies

In the UK in 2020, only 14 firms listed in the FTSE350 were headed up by female CEOs. UK companies with no women on their executive committees reported a net profit of 1.5% compared to a 15.2% net profit margin at companies with at least one in three women at the same level – a figure 10 times greater.

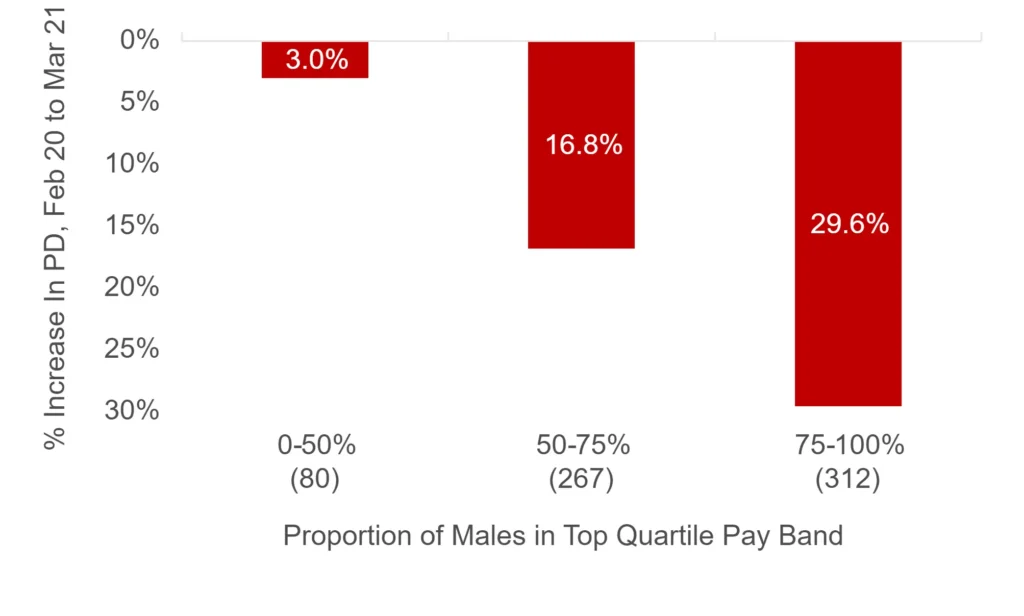

Figure 3 shows the increase in the probability of default (PD) for 659 UK companies from the beginning of the pandemic to a year on. The chart shows that the companies with a large proportion of men dominating the top quartile pay band deteriorated more severely during COVID-19. The firms with a minimum of 50% females in the top quartile pay band deteriorated on average by a modest 3%, compared to almost 30% worsening for the firms with 75-100% male top earners.

Figure 3: COVID-19 impact on top quartile pay band gender gap

These findings suggest that companies have much to benefit from championing diversity at the executive level, including lower credit risk and less potential of defaulting.