The U.S. Federal Reserve started the long process of normalizing interest rates in late 2015. But with the US economy growing by a lacklustre 1.6% in 2016, and inflation at a benign 1.3%, Yellen chose to wait a full year before the recent hike in December 2016. With President-elect Trump keen to change the composition of the Fed board, interest rate expectations for 2017 are for at least two, and possibly three hikes.

Bank views of U.S. corporate credit trends in 2016 echoed the cautious Fed stance, with all major industries showing an increase in average credit risk across a fixed sample of 300 Investment Grade obligors. This caution was probably driven by the growth outlook rather than specific concerns about interest rates; and further rate rises will probably have a limited direct impact on investment grade balance sheets, because many corporates have taken advantage of low rates to lock in long-term funding and build cash piles.

The largest proportionate increase was in Technology (+30%), closely followed by Healthcare (+26%), Consumer Services (+26%), and Oil & Gas (+25%). The smallest increases were in Telecommunications (+3%) and Utilities (+3%). There were modest increases in Basic Materials (+10%), Industrials (+11%) and Consumer Goods (+15%).

The sector outlook for 2017 will depend on the new, All-Republican Government. Protectionist measures may invite international retaliation but typically provide at least a short term economic gain. The steep rise in Healthcare credit risk in 2016 may be an early reflection of Republican aversion to ‘Obamacare’, but the proposed scrapping is already being watered down. The Oil & Gas industry has seen the West Texas oil price spike to finish up 45% over the past year, and OPEC are keen to maintain the current level. Trump’s Government is expected to encourage domestic and investment spending, and is already having some success with persuading US Corporates to rethink their factory location decisions.

With the new President taking office this month, the 2017 trends may soon look very different.

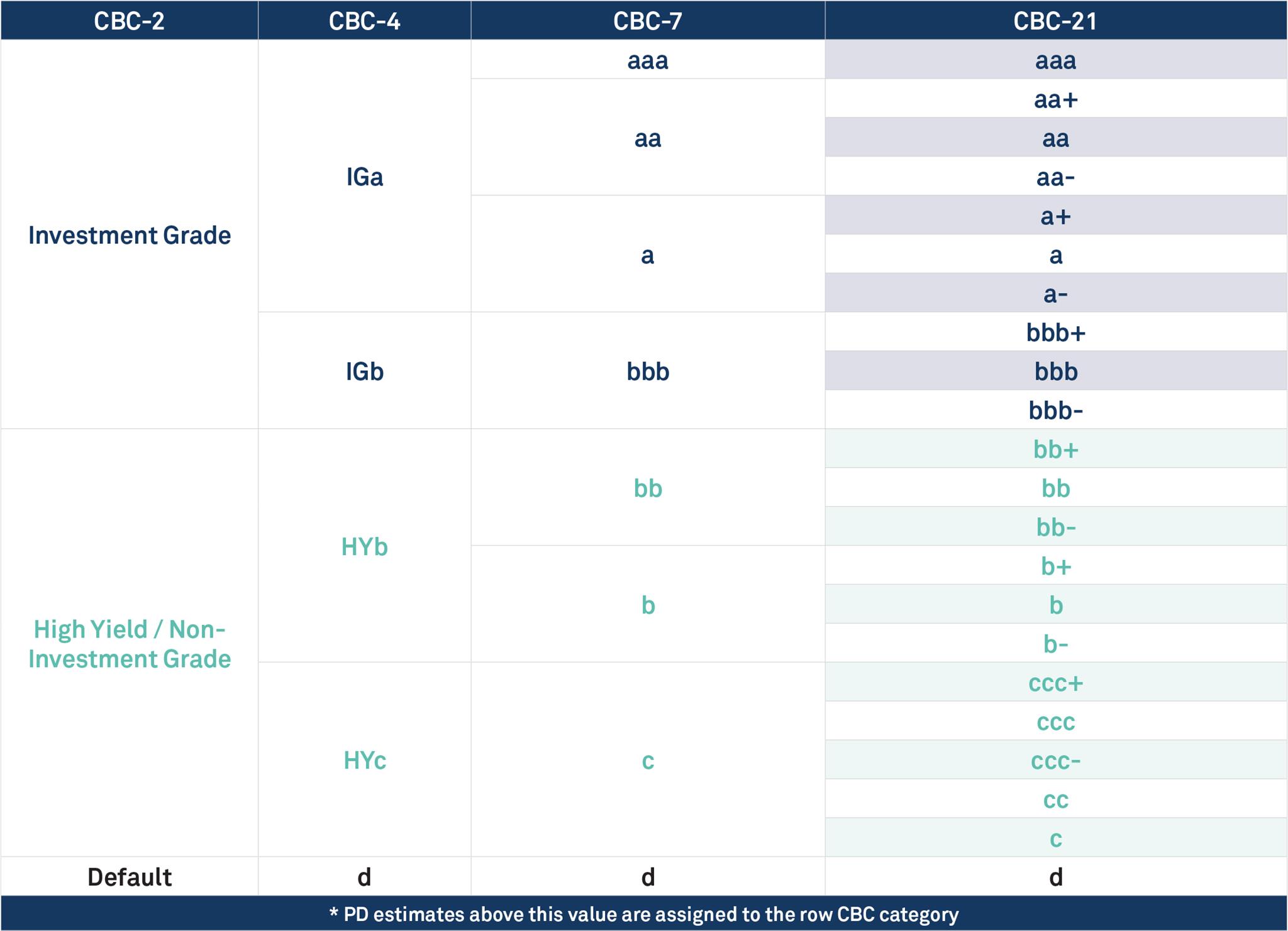

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

Image Source: Twitter.com

{kind=link}