Oil and Gas credit consensus isn’t following the price up

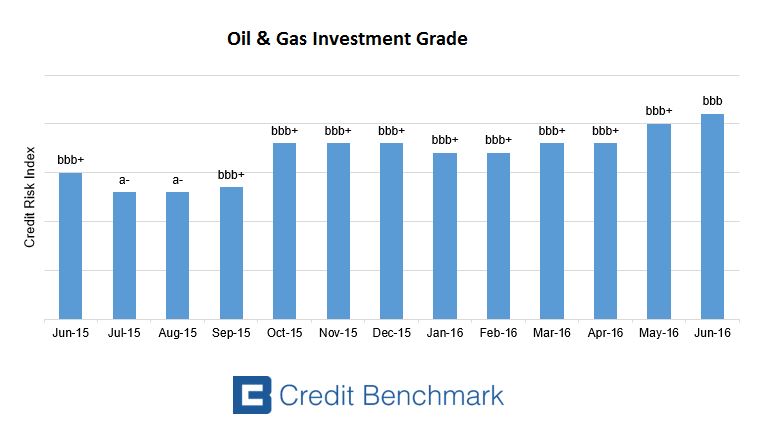

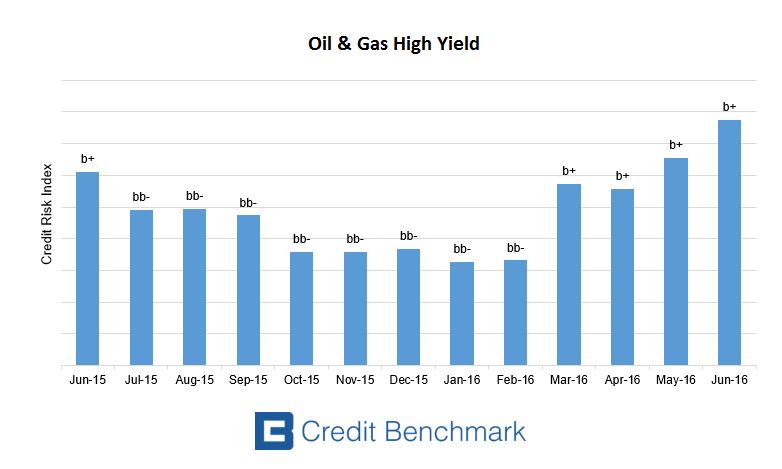

The oil price has been trending sharply upwards for most of 2016. Even with a 10 percent dip since the June high, Brent crude is up about 50 percent since the beginning of the year. U.S natural gas prices have also recovered, although somewhat more tentatively. These rises should be welcome news for lenders. But the Credit Benchmark consensus suggests that banks are still very cautious. The average CBC* rating for investment grade credits in the sector actually fell a notch between January and June, from bbb+ to bbb. In high yield, the average rating also dropped a notch, from bb- to b+.

Each company has its own story, of course, but there are several industry-wide trends which help explain why ratings have been moving in the opposite direction from prices.

For one thing, even after the rebound oil is less than half the price of the long stable period from early 2011 to mid-2014. The fall has been almost a sharp for natural gas, although prices for that commodity vary around the world. For high cost or highly leveraged oil and gas producers, the recent price increases only slow the pace of almost inevitable deterioration. No wonder that law firm Haynes and Boone counts $49 billion of debt in U.S. and Canadian oil and gas bankruptcies so far in 2016, and sees more coming.

Also, as lenders update their models, they are mostly factoring in a less prosperous future for this industry. The Saudi Arabian hegemony over the oil price looks increasing unlikely to return. Even if the kingdom once again becomes more willing to cut its own production, Iran and Iraq are both clamouring to increase their output and U.S. shale producers have shown a surprising ability to cut costs. It looks increasingly like oil will remain lower for longer. The gas oversupply might be even more durable, especially as alternative energy suppliers continue to eat away at demand from utilities.

The overall economy is not helping. Without increasing GDP, oil and gas consumption will be stagnant at best. But for most developed and developing countries, GDP growth estimates for this year ranges from disappointing to modest. The next few years also look duller than seemed likely even a year ago, even if politically induced economic disasters are avoided (for example a violent British exit from the EU or an erratic U.S. President Trump). For credit analysts, that points to more caution.

Still, the credit picture in this sector is much better than might have been expected from a quick look at the commodity price charts. Relatively few high cost producers have actually collapsed. In large part, the resilience reflects corporate caution during the good years. Investors and lenders did not back many projects which needed consistent triple-digit oil prices to survive. And when prices started to drop, the industry cut costs quickly and strongly.

The bankruptcies may keep coming for a while, but if the recent price rises are not a fluke, the oil and gas industry’s financial health could be close to a turn. The cbc, compiled monthly, offers a good way to keep up with current trends.

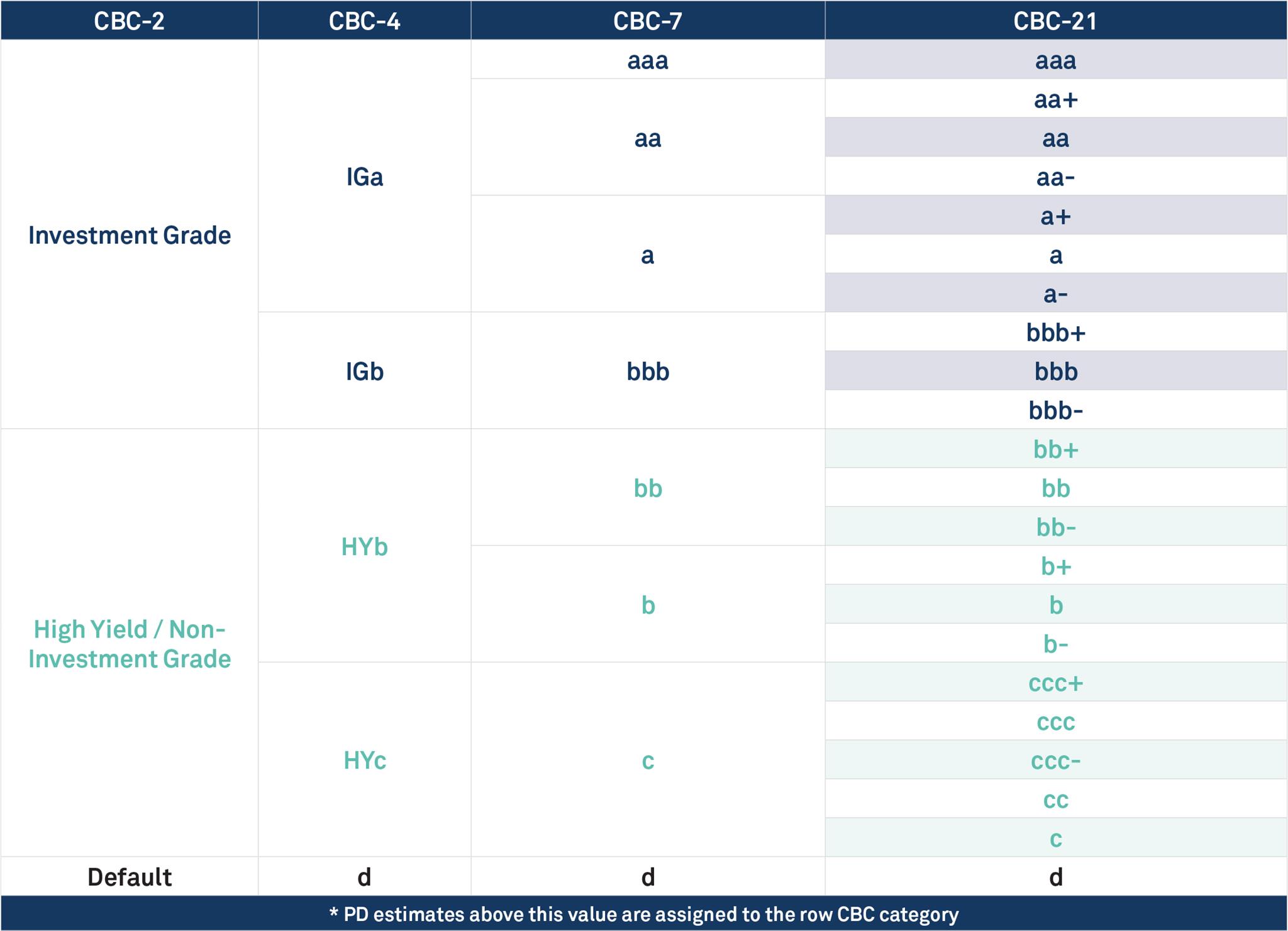

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of [bbb+] is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

{kind=link}