With the election looming, French bonds have been under increasing scrutiny. The spread of French 10-year government bonds over the equivalent German bund reached a four-year high of 90 basis points at the beginning of February, though it has been falling more recently.

The volatility of French government bonds only finds a faint echo in their CBCs*. At the beginning of 2016 the Sovereign CBC for France dropped one notch. It has since remained stable and the aggregate probability of default has been edging down after peaking last September. This broad pattern is repeated for significant public sector entities, issuers backed by the French state, such as Caisse d’Amortissement de la Dette Sociale (CADES) and Caisse des Dépôts (CDC), and is in line with the broader trend in modest improvements in sovereign credit risk across most of the EU. This improving trend is particularly noticeable in Greece.

The Brexit vote in the UK and the election of Donald Trump in the US surprised markets and since those upsets, markets have been wary of further signs of populist revolt against the political status quo. Bank sourced data can provide a clearer signal: in the run up to Brexit, the CBC was indicating a clear possibility of a “Leave” vote.

The strong showing of National Front candidate, Marine Le Pen, in opinion polls ahead of the first rouhttps://www.creditbenchmark.com/credit-benchmark…-brexit-concerns/nd of the French presidential elections on 23 April has had a direct impact on bond markets because of her anti-European Union stance and call for a return to the franc. Redenomination risk has been clearly signaled by the outperformance of [French] Model CAC bonds. These are bonds issued after 1 January, 2013, subject to collective action clauses which demand a super majority (75%) of investors to vote in favour of a change in currency denomination.

The gradual normalisation of French/ German sovereign bond spreads suggests markets are growing less concerned about Le Pen after the second round of the presidential election in May, and latest polls slightly favour Macron even in the first round.

Bank-sourced data can provide early warning of changing trends but equally, as appears to be the case in France, it may provide a stable signal and a more balanced view beyond the short term volatility of market reactions.

Image Source: FrontNational.com

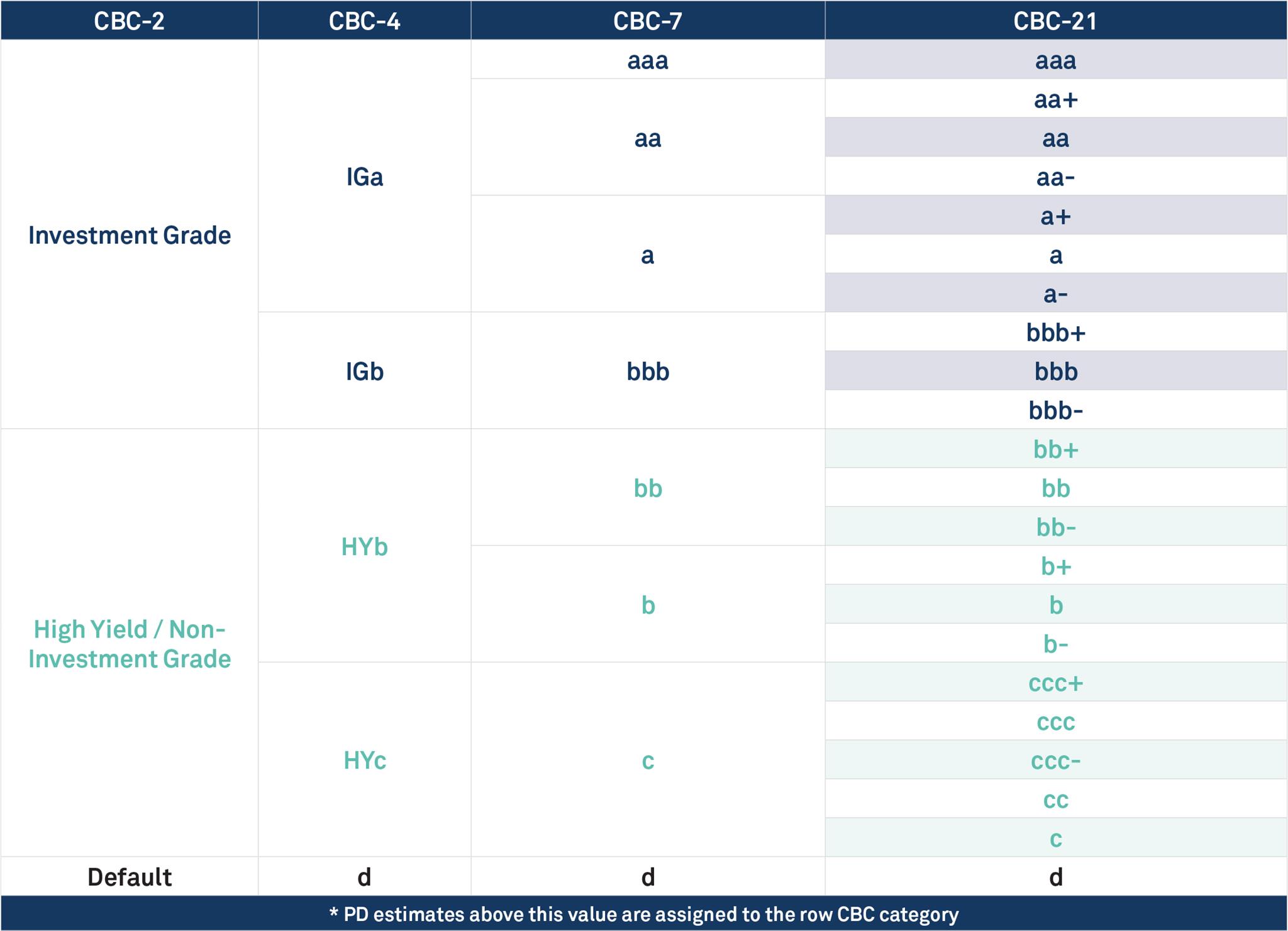

*CBC = Credit Benchmark Consensus; a 21-category scale which is explicitly linked to probability of default estimates sourced from major banks. A CBC of bbb+ is broadly comparable with BBB+ from S&P and Fitch or Baa1 from Moody’s.

Disclaimer: Credit Benchmark does not solicit any action based upon this report, which is not to be construed as an invitation to buy or sell any security or financial instrument. This report is not intended to provide personal investment advice and it does not take into account the investment objectives, financial situation and the particular needs of a particular person who may read this report.

{kind=link}